Tax and social policy engagement framework

- Executive summary

- Why we engage

- The current engagement framework – the Generic Tax Policy Process

- Model engagement process for policy reforms

- Exceptions

- Appendix 1: Overview of the Generic Tax Policy Process (1994)

- Appendix 2: Engaging with Māori

- Appendix 3: The DPMC Policy Project’s Start Right approach

- Appendix 4: Essential information for public engagement

Executive summary

1. Tax policy officials’ Tax and social policy engagement framework governs how engagement will be undertaken on tax policy issues and on the social policy initiatives that are delivered by Inland Revenue.[1] The purpose of this document is to affirm officials’ commitment to engagement and set out what stakeholders should expect from officials in undertaking engagement.

2. Since 1994, New Zealand has had a generic tax policy process (GTPP). A key feature of the GTPP is the focus on public consultation which plays an important role in creating and sustaining a tax system that is both widely accepted by taxpayers, and is able to respond to New Zealand’s changing needs. Consultation with stakeholders ensures that the alternative perspectives and expertise of those directly affected by the proposals are considered. This is necessary to improve policy and regulatory outcomes, and to ensure the durability of reforms.

3. This document reaffirms our commitment to the existing GTPP processes for all stages of policy development. Further enhancements to the process have also been implemented. These have been borne out of consultation on the way that the GTPP process has been working and aim to fill in the gaps identified and reflect how GTPP has evolved throughout the years.

4. Officials have committed to five principles for engagement which will be canvassed in greater detail in this document, these are:

- wider engagement;

- engagement with Māori;

- earlier and more frequent engagement;

- the use of a greater variety of engagement methods; and

- greater transparency and accountability.

5. Good faith engagement should be undertaken by all participants in the process.

Why we engage

6. The purpose of interacting with the public is to improve customer, policy and regulatory outcomes, and to inform stakeholders in advance of regulatory changes. Submitters will often have better access to information on the size and nature of the problem and how the issues can best be solved. Consultation can also enhance voluntary compliance because it allows interested parties more time to understand why there is a need to change, and more time to adjust to changes. Innovative solutions are most likely to come from working with those in the sector and using our tax system on a regular basis. There is an added sense of legitimacy and shared ownership if stakeholders have been given a chance to provide input into the development of new rules. Given the Government’s commitment to the Crown Māori relationship, consultation also serves a further purpose of facilitating appropriate engagement with Māori. This ensures that true and practical partnerships are developed with Māori stakeholders going forward.

7. Other practical benefits of consultation include:

- bringing alternative perspectives and the expertise of those directly affected by proposals;

- providing valuable input as to how realistic or practical a proposal is, as well as identifying potential unintended effects that policy makers have not considered;

- increased scrutiny of officials’ analysis and advice, allowing potential problems with a proposal to be identified and resolved early;

- helping regulators to balance opposing interests;

- increasing durability of reforms – better designed policies are less likely to need amendments once introduced;

- increased public buy-in and acceptance of changes, as stakeholders are more likely to accept proposals that they have been involved in developing; and

- improved understanding and increased compliance, reducing enforcement costs.

8. According to the OECD Background Document on Public Consultation,[2] there are three related forms of interaction or engagement with the public:

- notification;

- consultation; and

- participation

9. The three forms of engagement fall on a spectrum, with notification being the least amount of engagement and participation being the most. Notification involves a one-way flow of communication to the public of the Government’s regulatory decisions or plans. Consultation involves information flowing both ways between the public and the Government, and is concerned mainly with gathering information to facilitate the drafting of higher quality regulation. Participation refers to active involvement of interest groups in the formulation of government policy.

10. In tax and social policy consultation, we see the different forms of engagement as serving three purposes:

- Consultation to identify the policy problem or opportunity.

- Consultation or participation to help identify the best solution to a policy issue.

- Notification and some consultation of proposed changes to tax policy settings to the public as part of the democratic process.

The current engagement framework – the Generic Tax Policy Process

11. New Zealand has a tax policy process that is widely seen to work relatively well. Our formalised Generic Tax Policy Process (GTPP) includes a strong consultative component, and has a high degree of support from the private sector, tax officials, and government ministers.

12. In a 1994 report, the Inland Revenue Organisational Review Committee[3] stated that the GTPP’s main objectives were to:

- encourage early consideration of key policy elements and trade-offs;

- provide an opportunity for substantial external input into the policy formation process; and

- clarify the responsibilities and accountability of participants in the process.

13. These objectives are achieved through five phases:

- Strategic phases: high level economic strategy; fiscal strategy; revenue strategy.

- Tactical phases: rolling three-year work program; annual work and resource plan.

- Operational phases: detailed policy design; formal detailed consultation and communication; ministerial and Cabinet signoff of detailed policy.

- Legislative phases: drafting of legislation; ministerial and Cabinet signoff of legislation; introduction of bill; select committee phase; passage of legislation.

- Implementation and review phases: implementation of legislation; post-implementation review; identification of remedial issues.

14. There are opportunities for public engagement throughout these phases.

15. The strategic phase of the GTPP involves the development of an economic strategy, a fiscal strategy, and a revenue strategy. While no formal consultation processes are in place for this phase, broad policy proposals may be publicized through channels such as budget documentation.

16. In the tactical phase, targeted consultation takes place with the private sector and interested parties to identify the tax policy issues which are important to them, so that the government can prioritise which tax policy issues will be addressed over the next 18 months. Consultation on the development of the work program, combined with published information about the current work program, means that the public knows what changes are being contemplated.

17. In the operational phase, formal detailed consultation currently takes place during detailed policy design. On major reforms, consultation will often involve the release of a government consultation document. Normally, about six weeks are allowed for submissions (although sometimes this can take longer or shorter depending on the circumstances), and during the submission period officials have intensive face-to-face meetings with affected taxpayers. After the submissions have been received and considered, officials will report to the government on them.

18. The government may either decide to start preparing legislation taking into account what has been learned from submissions, or ask for further consultation on specific issues. This may involve direct consultation on specific points or the release of another consultation document seeking further submissions on those specific points.

19. In the legislative phase, Parliamentary Select Committees will consider submissions from the public as part of the legislative process. The Committee, on advice from officials, may then recommend that further changes be made in line with those submissions, or recommend that submissions be declined.

20. Tax policy advice in New Zealand is jointly provided by Inland Revenue and the Treasury. New Zealand is unique internationally in having the tax policy function being led by the tax administrator (Inland Revenue). Reviews of tax policy development processes across the world noted there are a number of advantages to having the tax policy function jointly led by the tax administration. The tax policy function is better informed by being closer to the coalface and benefits from greater intelligence flows. It also helps mitigate the risk of developing tax policy which is difficult to implement and enforce in practice.

21. The Treasury’s tax strategy team plays an important role in holding Inland Revenue’s policy advice accountable and providing an alternative view where they feel this is required. This arrangement increases the extent to which tax policy advice is tested internally before issues are put to Ministers or released for public consultation. The Treasury also play an important role in:

- ensuring tax policy is nested within a broader whole-of-government perspective;

- contributing an economic perspective to the development of tax policy; and

- ensuring the tax system is administered efficiently and effectively.

22. A consequence of the GTPP is that it increases the time it takes to develop and implement tax and social policy. The process also involves considerable time and resources for both the private sector and policy officials. However, most stakeholders believe the GTPP to be a valuable and essential part of building and maintaining a good tax system.

23. While recognising that current consultation processes under the GTPP generally work well, there is always room for further improvement. Officials are committed to improving the GTPP to ensure that the aims of GTPP are supported by our processes.

Outcome focused policy development process

24. Officials are committed to an outcome focused policy development process and will work more closely with customers, stakeholders and wider Government to ensure that business and customer input is sought at the various stages outlined below, as and when appropriate. Focusing on outcomes means that policy development will be an iterative process, with each stage not necessarily being strictly delineated from another. This process largely occurs in the operational and legislative phases of the GTPP, and is made up of seven overlapping stages:

- Problem/opportunity design: identifying issues and opportunities, clarifying the scope of the issue, and getting approval to begin project planning. This includes forecasting the time and resource required for the project.

- Solution design: undertake research and analysis to identify the options and solutions to address the issue, their costs and impacts.

- Public participation: this stage covers consultation, which will be genuine and fit for purpose depending on the nature of the policy issue.

- Ministerial decisions to proceed: policy options will be finalised, including the costs and impacts. Ministerial and Cabinet approval will be sought for the policy changes.

- Policy to legislation: initially draft legislation will be developed but this stage also covers the parliamentary process and any communication on resulting legislation.

- Policy to implementation of solutions: the legislation will be implemented and operationalised in accordance with the policy intent.

- Post implementation review: a post implementation review will be conducted to ensure that the policy works as intended.

25. Currently, consultation occurs only once the project has reached the public participation stage. This is when some research and analysis has already been undertaken on the issue, and options to address the issue have been identified. Some consultation also occurs in the policy to legislation stage through the Select Committee process.

26. We are committed to ensuring early and continuing engagement with the public on tax changes, and exploring new ways to broaden the public’s engagement with the development of tax policy.

27. We propose a new policy process, where practicable, where public engagement begins from the problem and opportunity design stage and continues throughout all seven stages, including post-implementation review.

Model engagement process for policy reforms

28. The proposals below are intended to reaffirm our commitment to existing GTPP consultation processes for each stage of policy development. They also seek to formalise further enhancements to current processes where gaps have been identified, and to reflect how the GTPP has evolved through the years.

29. This document is intended to formalise many principles and processes that are already being applied in major policy reforms, and also to ensure that the tax policy process is consistent with the Department of Prime Minister and Cabinet’s best practice guidelines for policy development.[4] It is intended that they will apply formally across the board following public feedback on our proposals.

30. Officials are committed to the following principles for all policy reforms:

- wider engagement;

- engagement with Māori;

- earlier and more frequent engagement;

- the use of a greater variety of engagement methods; and

- greater transparency and accountability.

31. The need for flexibility in managing issues, timing, and resource needs will affect the scope for consultation on a case-by-case basis. Therefore, the proposed processes outlined are not intended to be a prescriptive model of consultation to be strictly followed in all cases – there will be situations where a departure from the model process is justified.

Wider engagement

32. The project planning process for new policy issues will focus on ensuring that a range of stakeholders and skills are included in project teams from the start. This selection process will consider the particular expertise that is required, while ensuring that the groups most affected by the proposal are adequately represented.

33. This includes ensuring adequate representation as appropriate from interested parties across:

- Inland Revenue and the Treasury;

- other Government departments;

- tax professionals;

- accounting software providers;

- not-for-profit and other community organisations;

- industry and sector representatives; and

- members of the general public.

34. The level of engagement with these stakeholders will vary depending on the nature of the issue and the time and resource available. For some policy initiatives, engagement with the tax practitioner community may be sufficient. However, in areas like social policy and not-for-profit tax issues, wider engagement will be necessary. We think that wider engagement outside of the tax community will be most beneficial in the following circumstances:

- the tactical phase of the GTPP to help set the general direction of tax and social policy reforms;

- when attempting to understand the policy problem or opportunity;

- when understanding with who and how to engage; and

- when attempting to understand the potential impact of proposed policy changes.

35. We are committed to identifying and developing strong links with interested stakeholders in these areas and using them effectively, while acknowledging that it may take some time to develop.

36. Once identified, the interested parties should be able to be engaged at every stage of the policy development process. At a minimum, this will involve communication of relevant decisions and proposed processes going forward. Where appropriate, opportunities for co-production of tax policy with a wider range of stakeholders involved from the start will lead to more robust and durable policy outcomes.

37. Engagement on matters beyond purely tax technical policy issues will also be more effective if those who will have to administer and implement policy decisions can provide early input. This will help identify what the feasible options are, and inform design decisions to ensure that new tax rules are as easy to comply with as possible.

38. Wider engagement also means that, where appropriate, we will seek feedback on a wider range of policy products. Draft wording for inclusion in legislation, commentaries, and Tax Information Bulletin (TIB) items are examples which could benefit from prior consultation before they are finalised or released. Where appropriate, and where time permits, consultation on elements of draft legislation will help ensure that the legislation achieves the policy intent and resolves any inconsistencies. Draft commentaries and TIB items can also be consulted on to ensure they accurately communicate the policy intent, and submitters could suggest areas in which further guidance would be helpful.

Engagement with Māori

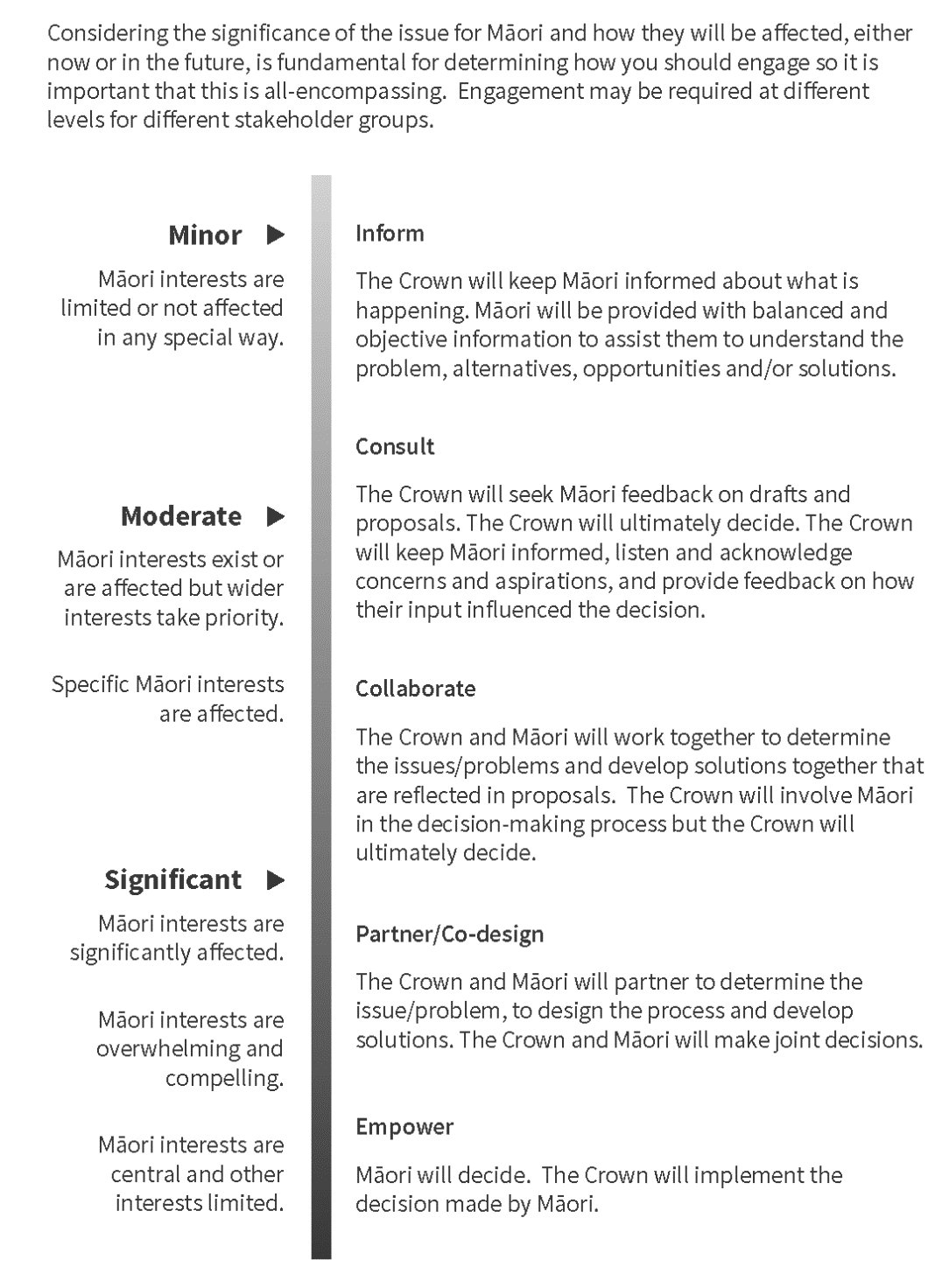

39. As part of the initiatives towards wider engagement, it is important that appropriate weighting is given to the status of Māori as rightsholders in the process and as Treaty partner of the Crown. To give effect to this special relationship, officials intend to adopt the Māori Crown Relations framework endorsed by Cabinet.[5] The intent and values for engaging with Māori are set out in Table 1.

| Area for consultation | Proposed detail | |

|---|---|---|

| Intent | To work with Māori to respond better to the range of needs, aspirations, rights and interests and provide for active partnership with Māori in the design and implementation of the process and outcomes sought. | |

| Values | Partnership | The Crown and Māori will act reasonably, honourably and in good faith towards each other as Treaty partners. |

| Participation | The Crown will encourage, and make it easier for Māori to more actively participate in the relationship. | |

| Protection | The Crown will take active, positive steps to ensure that Māori interests are protected. | |

| Recognition of cultural values | The Crown will recognise and provide for Māori perspectives and values. | |

| Use mana-enhancing processes | Recognising the process is as important as the end point; the Crown will commit to early engagement and ongoing attention to the relationship. | |

40. The way that engagement is conducted with Māori will also be determined by the matrix set out in appendix 2. As part of the Māori Crown Relations framework, this matrix provides a sliding scale that stipulates the level and type of engagement required depending on the extent of Māori interests involved.

Early and frequent engagement

41. Our stakeholders have identified earlier engagement as a key area where there is room for improvement. Earlier engagement helps to refine the problem definition and identify what might be plausible solutions. This may result in the need for less consultation later in the policy development process, as many of the issues will already have been worked through before the details of the proposals are consulted on. It can also help with appropriately scoping the project early on, which can help policy officials to more efficiently allocate policy resources.

42. We think the first step to engagement is to establish strong links with interested parties. Where possible, standing committees could be formed for various issues or sector groups. Or if such groups have already been formed by other government agencies, those existing relationships could be shared between government agencies as necessary. Tax policy officials already have established consultation channels with representatives of large businesses, but this could be extended to representatives of small and medium businesses, not-for-profit organisations, and other sector or industry groups.

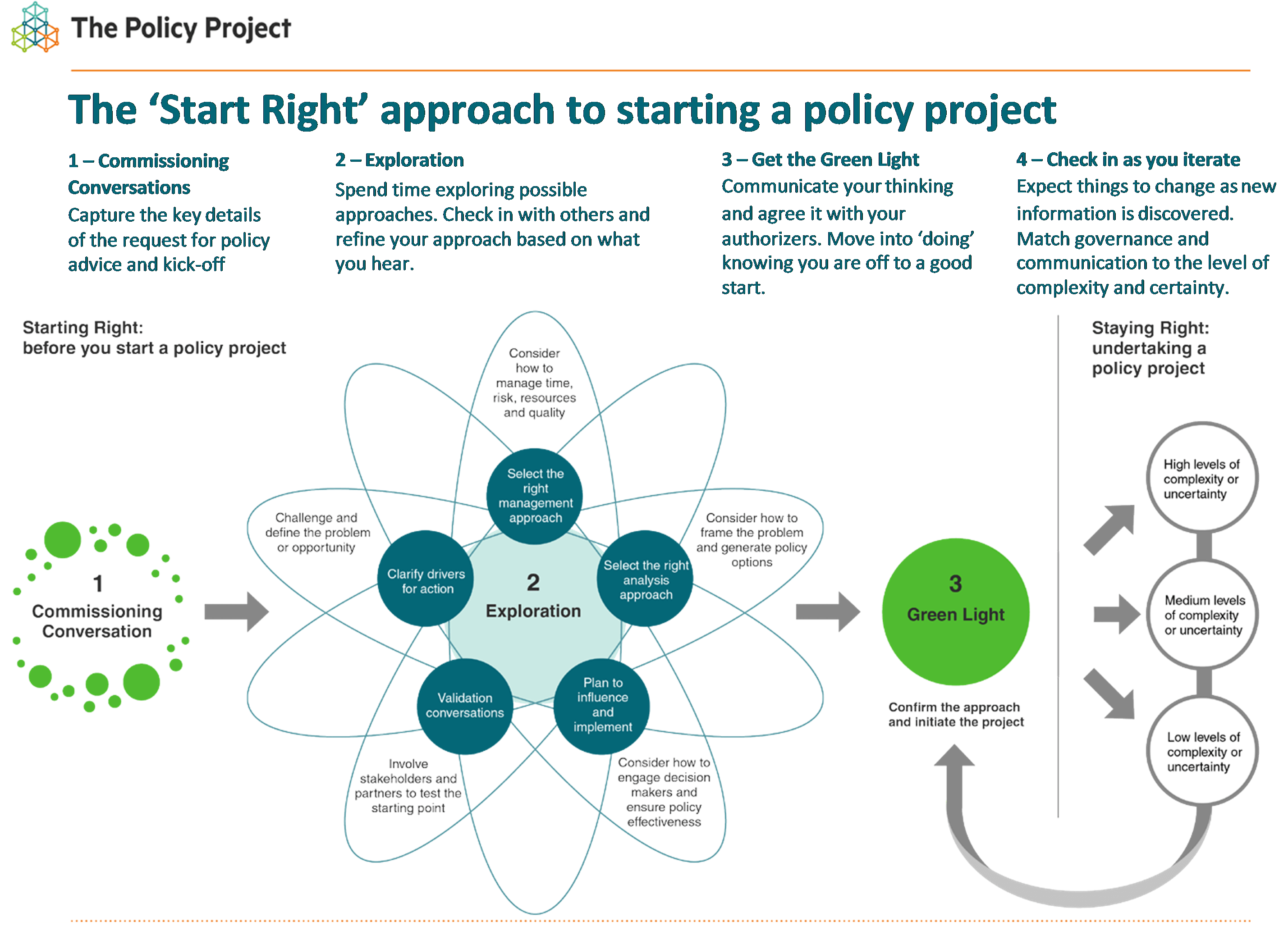

43. Public engagement should be seen less as one discrete task or step in the policy development process – rather, officials will be engaged in continuous ongoing dialogue with interested parties. This will provide opportunities for the public to raise issues as they arise, and it will facilitate more frequent engagement as interested stakeholders have already been identified. We expect that engagement will be spread out over the course of the policy development process, and that it will become part of a more iterative process. This is consistent with the Start Right approach to policy development proposed by the Department of the Prime Minster and Cabinet (DPMC) Policy Project (see appendix 3).

44. The public will be notified on what the Government is working on or intending to work on. This already occurs for most policy issues through the publication of the Government’s tax policy work programme (TPWP), which is refreshed every 18 months.

45. The Ministers of Finance and Revenue are responsible for setting and agreeing the Government’s TPWP every 18 months. Setting the TPWP involves engaging with Ministers and stakeholders towards the end of each TPWP cycle to ensure that the right mix of items are included on the refreshed TPWP, taking into account factors such as wider Government priorities and objectives as well as initial stakeholder views. Once a new work programme is set, we intend to regularly update the TPWP (as appropriate). This includes, for example, ensuring that deliverables for key items of work are progressing within the timeframes outlined on the TPWP. This will also involve checking in with Ministers to ensure that they are still comfortable with the relative priorities of the items on the TPWP, or understanding whether expectations for certain items of work may have changed.

46. Officials are also developing processes to communicate the Government’s remedial work programme, and to provide interested parties (such as the tax practitioner community) with the opportunity to identify remedial issues which should be addressed. Where appropriate, this will allow engagement on a review of the effectiveness of policies that have been implemented and address any gaps in the rules.

47. We recognise that engaging with policy issues and making submissions comes at a cost to submitters, as often a significant amount of resource is dedicated to preparing submissions. However, we think it will reduce the amount of resource needed to analyse more detailed policy options later in the policy process. Those who do not wish to participate in the earlier engagement with officials to scope the problem definition are free to decline, and instead engage later when more detailed policy options are presented.

Methods of engagement

48. For significant policy changes, there will be at least one round of formal public consultation. This already occurs for the vast majority of projects and will continue. However, a greater focus will be placed on ensuring that the method of engagement used is fit for purpose. While a consultation document may be appropriate in most circumstances, officials will consider:

- the intended audience and how best to communicate with them;

- who is likely to be affected by the proposal;

- the scope and scale of the proposal; and

- the purpose of the consultation.

49. Some alternative engagement tools include the use of:

- focus groups with customers;

- workshops with representative industry bodies, community organisations, market participants, and service providers;

- online forums;

- use of multimedia content across different languages;

- processes that are culturally appropriate for particular groups of people – for example, using a hui to engage with Māori customers; and

- face to face discussions with affected customers.

50. Many of these alternative engagement tools facilitate active participation by stakeholders, in some respects co-producing the policy solution. Officials will need to weigh up the time and cost required for each engagement tool, and what outputs are created. This will then be incorporated into officials’ project planning processes. Different engagement tools will be added to this list as and when they become more commonly used.

51. When consultation takes place, officials will ensure that the scope of the consultation is clearly communicated. It should be clear what has already been decided, and what scope there is left to influence the outcome.

52. The use of confidential consultation will be minimised in order to ensure that consultation is transparent, and all interested parties have an opportunity to participate.

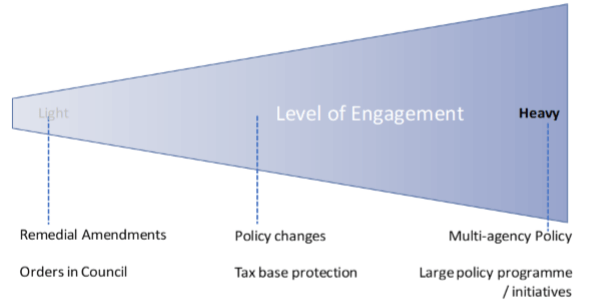

53. Consultation is not a ‘one size fits all’ approach. The level of engagement undertaken will be commensurate to the nature and complexity of the policy issue.

Figure 1: Level of engagement

Transparency

54. The Organisational Review Committee recognised that consultation must be, and be seen to be, genuine. Genuine consultation is a two-way flow of information, and this should include another flow of information back to submitters. This will be better achieved through a more transparent process to feed back to submitters how officials have considered their points, whether any changes have been made to proposals as a result of their submission, and why or why not. Ensuring that consultation is genuine supports the Tax Working Group’s recommendation that engagement on tax policy initiatives be carried out in good faith by all participants.

55. Following consultation, feedback will be provided to submitters to communicate the Government’s response to the submissions. This would note what has changed as a result of the consultation, and why or why not.

56. Feedback will be provided in a timely manner, once policy decisions have been made. If this is not achievable, officials will provide an explanation of why this is not possible.

57. Under existing processes, officials report to Ministers once submissions on a proposal have been received. This will include a summary of the submissions, as well as recommended responses to those submissions. Cabinet Office Circular CO 18(4), as part of providing for the proactive release of Cabinet papers, also suggests that related key advice papers can be proactively released at the discretion of the relevant Minister. Officials support the release of these key advice papers where appropriate. Releasing existing information also means that this could be achieved without much more additional resource being required to achieve this greater transparency.[6]

58. However, this proactive release would be subject to certain legal or other practical requirements – for example, if the release of the information would adversely affect the integrity of the tax system. Requirements under the Official Information Act 1982 will also be considered when deciding whether to release certain information.

Remedial issues

59. The purpose of a remedial amendment is to ensure that tax legislation aligns with the original policy intent. As the policy would have been through a full consultation process before it was enacted, the value added by consulting on remedial issues is more limited.

60. However, some targeted consultation will help ensure that remedial amendments:

- achieve the desired policy outcome;

- are able to be easily applied (is the legislation clear and unambiguous?);

- do not increase compliance or administration costs; and

- do not have any unintended consequences.

61. It should be made clear that the policy is settled and only details concerning the above four matters are subject to consultation. So far, these matters have been left until Select Committee to be ironed out, as they mostly concern how the legislation has been drafted. However, in some circumstances it would be beneficial to use some form of limited consultation to test the practicality of proposed solutions and to gather relevant data.

Exceptions

62. While we recognise the importance of providing a clear and transparent set of principles on which consultation processes should be based, we think it is important that processes have enough flexibility to adapt to unique circumstances. There will be some circumstances where full consultation is not appropriate or possible given the costs and benefits associated with engaging on that particular issue. However, the government and policy officials will ensure that these exceptions to usual consultation processes are only allowed on a principled basis.

63. For example, under GTPP there is generally an exception to wide public consultation for revenue protection or anti-avoidance measures. This is because prior consultation on these measures could provide taxpayers the opportunity to rearrange their affairs prior to the enactment of the proposed measures. This would reduce the amount of revenue collected.

64. Other circumstances where wide public consultation may be inappropriate include measures included as part of the Budget process, or where Inland Revenue’s secrecy obligations under the Tax Administration Act 1994 (or other secrecy obligations under another Act) may prevent officials from undertaking wider consultation. For example, if there are proposals developed in response to a case involving a specific taxpayer or group of taxpayers, it may be inappropriate to consult widely in order to protect those taxpayers’ commercial position.

65. Urgent Government priorities may sometimes require a more truncated policy development process. However, the principles of earlier and wider engagement and greater transparency will still be adhered to, where appropriate, but adapted to suit the tighter timeframes.

66. The reason for having exceptions to the full GTPP consultation process is to ensure that consultation processes are flexible and not overly prescriptive. As such, the exceptions listed in this document are not intended to form an exhaustive list.

67. As a general rule however, it is our view that exceptions will be used sparingly, and the reasons for departing from the usual level of engagement required by the GTPP should be communicated to the public once the proposals are in the public domain. This is to promote greater transparency and accountability, and to ensure that the reasons given for departing from the GTPP can be subjected to public scrutiny.

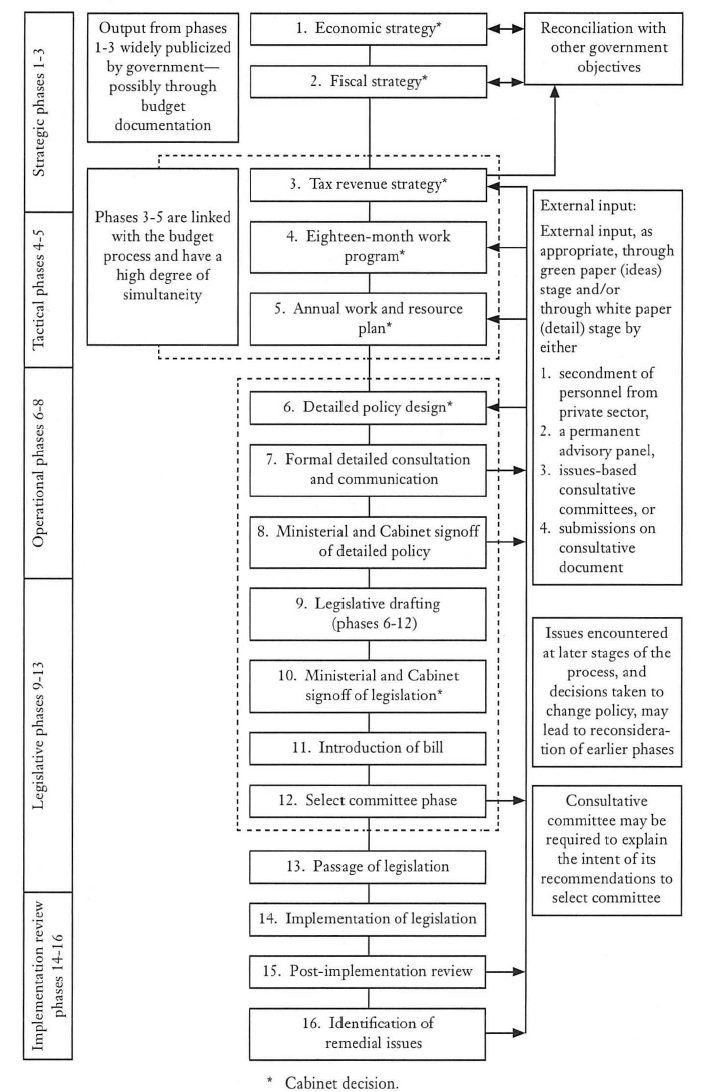

Appendix 1: Overview of the Generic Tax Policy Process (1994)[7]

Figure 2: The Generic Tax Policy Process

Appendix 2: Engaging with Māori

Figure 3: How to engage[8]

Appendix 3: The DPMC Policy Project’s Start Right approach[9]

Figure 4: The ‘Start Right’ approach to starting a policy project

Appendix 4: Essential information for public engagement

| Item | Description |

|---|---|

| Subject of the consultation | A brief (one to two paragraph) synopsis defining the problem or opportunity, and what points officials are seeking feedback on. |

| Scope of the consultation | What decisions have already been made, and what is still able to be influenced by the consultation (that is, whether we are seeking views on what the problem or opportunity is, or only on policy options). |

| Intended audience | If there are any interest groups or sectors in particular that the document is aimed towards. |

| Duration of the consultation period | The closing date for submissions should be provided, and should be no less than six weeks except in exceptional circumstances (and those circumstances should be clearly outlined in this section). |

| Lead official | Name and contact details of the lead official. |

| Additional ways to be involved | For example, meetings between interested parties and policy officials. |

| Next steps following the end of the consultation period | This should briefly set out the milestones following the end of the consultation period – for example, when officials plan to report to Ministers, when feedback on submissions will be released, or whether a further round of consultation is planned. |

| Historical context and previous engagement | A brief (one paragraph) summary of how the issue arose, and a comprehensive list of the prior engagement to date (including title and date of past consultation documents). |

[1] The social policy initiatives administered by Inland Revenue include KiwiSaver, student loans, child support and Working for Families Tax Credits.

[2] Background Document on Public Consultation, OECD, 2006, https://www.oecd.org/mena/governance/36785341.pdf

[3] Organisational review of the Inland Revenue Department: report to the Minister of Revenue (and on tax policy, also to the Minister of Finance) from the Organisational Review Committee, April 1994.

[4] Start Right, DPMC Policy Project, https://dpmc.govt.nz/our-programmes/policy-project/policy-methods-toolbox/start-right. See Appendix 3: The DPMC Policy Project’s Start Right approach.

[5] https://tearawhiti.govt.nz/te-kahui-hikina-maori-crown-relations/engagement/

[6] This is also consistent with the proactive release of Cabinet papers within 30 business days of a Cabinet decision being made. The proactive release of Cabinet papers started on 1 January 2019 – see https://www.beehive.govt.nz/release/government-proactively-release-cabinet-papers-%E2%80%93-and-open-government-action-plan-be-issued.

[7] Organisational review of the Inland Revenue Department: report to the Minister of Revenue (and on tax policy, also to the Minister of Finance) from the Organisational Review Committee, April 1994, page 81. Note that the GTPP has evolved over the years so what is contained in this diagram may not fully reflect current consultation practices.

[8] Crown engagement with Māori framework, https://tearawhiti.govt.nz/assets/Maori-Crown-Relations-Roopu/451100e49c/Engagement-Framework-1-Oct-18.pdf

[9] Start Right Guide, DPMC Policy Project, February 2018, https://dpmc.govt.nz/publications/start-right-guide.