New Zealand’s taxation framework for inbound investment

A draft overview of current tax policy settings

Contents

- Principal conclusions

- Introduction

- Main features of the taxation of inbound investment

- The impact of taxation on foreign direct investment

- The company tax

- Non-resident withholding tax (NRWT) on interest on related-party debt

- Debt and equity advanced by a foreign parent and thin capitalisation provisions

- Deviations from normal rules, marginal investors and welfare implications

- BEPS

- Unrelated-party debt and NRWT/AIL

- Conclusions

- Appendix

Principal conclusions

This paper presents an overview of New Zealand’s framework for taxing income earned on inbound investment. It is intended to provide a context for discussions of recent and prospective changes to the taxation of such income.

Developing a framework for taxing inbound investment is not a simple exercise. It involves making judgements, balancing a variety of factors that can point in different directions. The impact of taxes on the pre-tax cost of capital is one but only one of a number of important factors that must be taken into account. For example, it is important that the taxation of inbound investment fits within a coherent national tax system.

New Zealand has had a series of reviews over the last couple of decades that have examined the issues from a variety of points of view and have, in the end, resulted in the present framework. This paper reflects that accumulated thinking. While the analysis is complicated, it arrives at some clear conclusions. These conclusions are not cast in stone; if circumstances changed in the future, they would need to be reconsidered.

The company tax is the principal tax applying to inbound investment. Its structure is broadly consistent with international norms, while having features designed to respond to New Zealand’s particular economic and institutional context. International consistency simplifies the interaction of New Zealand’s tax system with those of other countries.

The principal conclusions of the paper may be summarised as:

- It is in New Zealand’s interest to levy company income tax and non-resident withholding tax (NRWT) on income from activities carried on within New Zealand’s borders. These taxes are broadly consistent with international norms, and provide significant funding for Government priorities and programmes that would otherwise be needed to be raised elsewhere.

- Base-protection measures, such as thin capitalisation and transfer pricing rules, are sensible to protect the tax base and ensure that New Zealand gets its fair share of revenues.

- There is a continuing case for NRWT on interest from related-party debt to supplement the company tax and to play a role in determining New Zealand’s share of taxes on activities within its borders.

- Deviations from normal tax rules, intended or otherwise, can lead to substitution of low-taxed investors for tax-paying investors, reducing national income without necessarily lowering the overall pre-tax cost of capital to New Zealand or increasing investment. Accordingly, base-maintenance provisions that ensure the intended level of tax is collected will often be in New Zealand’s best interest.

- NRWT on portfolio debt has been modified by the approved issuer levy (AIL) to provide relief from taxation in circumstances where it is in New Zealand’s interest to do so. On balance, continuing with New Zealand’s AIL/NRWT system for third-party debt is likely to be in New Zealand’s best interest.

There are a number of future base erosion and profit shifting (BEPS)-related issues that New Zealand will be considering. The OECD has estimated that between 4% and 10% of global corporate income tax revenue is lost as a result of BEPS. While New Zealand is starting from a good position relative to many other OECD countries, taking further steps to address BEPS is an important Government priority.[1]

Design of policy approaches should reflect the framework outlined above. At the same time, they should be consistent with maintaining New Zealand’s position as an attractive location to base a business. There are costs and benefits in making tax policy changes in this area and it is important that changes here are carefully worked through.

Introduction

New Zealand relies heavily on inbound investment to fund its capital stock. Taxes can have important effects on the incentives for non-residents to invest in, or lend money to, New Zealand. It is important that New Zealand has a considered framework for the taxation of the income of non-residents earned here. The purpose of this paper is to outline New Zealand’s framework for taxing income from inbound investment and to discuss some of the considerations that are important when assessing the desirability of policy changes in this area.

A priority for the Government is ensuring that New Zealand continues to be a good place to invest and for businesses to be based, grow and flourish. Excessive taxes on inbound investment can get in the way of this happening. It is also important that inbound investment takes place in the most efficient ways. Poorly designed taxes can hamper investment from occurring in the ways which provide the best returns to New Zealand.

Taxes are necessary to fund government spending. New Zealand faces growing fiscal pressures with an ageing population. Maintaining robust tax bases is important to reduce upward pressures on tax rates and help maintain our coherent tax structure.

New Zealand levies tax on the profits of non-resident-owned firms that are sourced in New Zealand. These taxes should not be voluntary. Tax rules should not allow foreign-owned firms to sidestep paying taxes on their profits in New Zealand.

Almost all taxes are likely to have some negative effects on economic activity. In setting taxes on inbound investment there is a balance to be struck. Taxes should not unduly discourage inbound investment but we want the tax system to be robust. It is important that taxes are fair and seen to be fair.

It is helpful to start by defining some terms as clearly as possible. By the “pre-tax cost of capital” we mean the minimum pre-tax rate of return required to attract investment. Some commentary on some recent and possible future base-maintenance tax changes has raised the concern that they could increase the pre-tax cost of capital to New Zealand and questioned whether they are consistent with New Zealand’s taxation framework. The paper does not examine these specific measures. Its purpose is to outline New Zealand’s tax framework for inbound investment more generally, and provide background for discussions of the effects of recent and prospective changes, including on the pre-tax cost of capital.

A framework for the taxation of income from inbound investment

The framework for the taxation of inbound investment has been driven by many considerations. It is part of a tax system which has the overarching goal of maximising the welfare of New Zealanders. More specifically, it seeks to accomplish that goal by:

- ensuring that taxes levied on the investment income from inbound investment raise revenue to fund government priorities and programmes in a way which is as fair and efficient as possible;

- ensuring that, within widely accepted international norms, New Zealand gets its fair share of tax revenue from activities carried on within its borders;

- ensuring that New Zealand remains an attractive place to invest and base a business; and

- minimising distortions caused by taxation so that investments are financed in ways that are most efficient and undertaken by those who can do so most efficiently.

There are inevitably trade-offs among these objectives.

A history of reviews

Over the last 15 years, New Zealand tax rules have been subject to a succession of reviews, including:

- McLeod Review

- Business Tax Review

- International Taxation Review

- Capital Market Development Taskforce

- Savings and Investment Review

- Tax Working Group, and

- numerous investigations within Treasury and Inland Revenue.

In the end, substantial changes have been made to the taxation of income from outbound investment. The system applying to inbound investment has been stable in concept and overall design, while subject to refinements designed to respond to the considerations outlined above. These have included changes to banking thin capitalisation rules, changes to the broader thin capitalisation rules in 2010, two cuts in the New Zealand company tax rate, as well as recent measures applying to the NRWT and thin capitalisation rules. Further changes may result from New Zealand’s response to the BEPS project at the OECD. The recent and on-going work in this area maintains the current paradigm, while constantly striving to respond to changing economic circumstances and make improvements at the margin.

As a consequence of the recent history of reviews, we are not embarking on another zero-based review of sweeping alternatives. For example, we see no benefit in reviewing yet again whether New Zealand should adopt a Nordic dual income tax system or an Allowance for Corporate Equity (ACE) company tax system.[2] However, it is important to maintain a dialogue to discuss specific issues to ensure that any changes are consistent with our tax settings and with the best interests of New Zealand. This paper has been prepared to assist in that dialogue going forward.

General considerations

There are many factors, some inherently unquantifiable, that are relevant in choosing the “best” tax system for New Zealand. They must be balanced by making judgements based upon experience, taking into account insights offered by the economics profession. New Zealand’s tax system is a product of a long process of such thinking and trade-offs, as illustrated by the list of reviews.

Optimal taxation

We do not consider that the economic literature is at a stage where there is an obvious best way of taxing the income from inbound investment. There are economic models where it is optimal for a Small-Open Economy (SOE) such as New Zealand to levy no tax on inbound capital. However, as is discussed further below, these models typically rest on strong simplifying assumptions that make them an inadequate guide for dealing with many of the most important tax policy issues New Zealand faces. They tell us what might be optimal if there are no “economic rents” (so all investments end up earning exactly the same pre-tax rate of return) and if there is “perfect capital mobility” (so New Zealand can obtain as much capital as it wishes at a completely fixed interest rate). However, in practice there may be important economic rents associated with doing business in New Zealand (so-called “location-specific economic rents”) and this overturns the “no tax” conclusion. Also while capital imported into New Zealand is likely to be highly mobile, it is probably less than perfectly mobile.

The models often assume that there is a single form of capital. This makes them peculiarly unsuited to examining many important policy issues such as the tax and national welfare effects of a foreign parent company replacing equity with debt or the effects of taxes affecting which types of foreign investor choose to invest in New Zealand.

There are also many important objectives of our company tax system that are not incorporated in these models, such as supporting the coherence of our personal tax system.

The bottom line in drawing this together is that there is no textbook we can consult for a reliable “optimal” way of taxing inbound investment. Pragmatic judgements and trade-offs are required.

What is a competitive tax system?

It is sometimes argued that New Zealand must parallel developments elsewhere in order to have a “competitive” tax system. For example, that company tax rates must follow international trends or New Zealand should mirror an incentive offered by another country. While there can be some advantages of consistency with other jurisdictions, if other countries subsidise certain forms of production, it will generally not be in New Zealand’s best interests to match the subsidies. The overseas subsidies may change world prices but it will generally be best for New Zealand to produce as efficiently as it can given the prices it faces.

New Zealand enhances its competitiveness when it has a tax system that encourages the most productive use of its resources. This is likely to be largely although not completely independent of foreign company tax rates or special incentives that may be offered abroad.

The McLeod Review discussed the concept of competiveness in its Final Report. It noted that tax incentives for certain activities are sometimes advocated on the grounds of increasing competitiveness and that providing an incentive to some specific activity (perhaps for firms that export or for firms producing import substitutes) will tend to increase investment in that activity. But that will generally divert scarce labour and capital resources away from other activities. Subsidising one activity can mean a surtax on other activities. New Zealand is likely to be best off if it focuses on where it has a comparative advantage. Industries that survive international competition without special incentives are most likely to reflect New Zealand’s comparative advantage.

A general cut in the company tax rate is sometime advocated on the grounds of competitiveness. Other things equal, a cut in the company tax rate will encourage inbound investment. But cutting the company tax rate can provide windfall benefits to those who have invested in New Zealand in the past. It can also provide windfall benefits to those who will invest in the future whether or not there is a tax cut. It will reduce tax collections and, for a given level of government spending, this will put upward pressure on other tax rates. These other taxes may be more costly to New Zealand than the taxes forgone.

A coherent tax system

Overall, it is fair to say that New Zealand’s tax structure is broadly consistent with international norms and well within the bounds of what is reasonable. New Zealand has a coherent and stable tax system which adds to business certainty. Its broad-base, low-rate (BBLR) approach minimises distortions and promotes economic efficiency. Having a company tax rate which is not too far away from higher rates of personal tax helps maintain the integrity of the personal tax system. When examining the effects of taxes on inbound investment the implications of any changes for the tax system as a whole need to be kept in mind.

Maintaining a robust company tax base raises substantial revenue, helping to keep other tax rates (such as for personal tax and GST) as low as possible. Other taxes, including those on personal income, can have an impact on foreign direct investment (FDI). New Zealand’s low top personal rate, imputation system, lack of a capital gains tax and consistent and coherent tax settings all help New Zealand to be a good place for entrepreneurs to live and base a business. Having a robust company tax also helps New Zealand in avoiding a host of inefficient taxes that are common in other countries, including stamp duties and other taxes on transactions.

We consider that future reforms affecting the taxation of inbound investment are likely to be “at the margin” changes rather than a wholesale overturning of the current approach.

Main features of the taxation of inbound investment

Inbound investments can be either direct or portfolio. The two main taxes that apply to inbound investment are the company tax and the NRWT/AIL. These taxes can affect incentives for both direct and portfolio investment into New Zealand.

A key tax on both direct and portfolio inbound equity investment is the company tax that is applied to income earned in New Zealand by direct investors. New Zealand’s company tax is consistent with international norms. The tax applies to income arising from New Zealand sources. The main guiding principle is BBLR, which avoids tax incentives and applies a single company tax rate across a broad definition of taxable income. BBLR is intended to minimise the distortionary costs of taxation. Partly as a consequence of this broad tax base, New Zealand’s share of company tax revenues as a percentage of GDP is fourth highest in the OECD, (4.4% of GDP compared with the OECD average of 2.9% in 2013).[3] Thus, company tax is an important tax base for New Zealand. New Zealand has implemented a number of measures, such as thin capitalisation rules, to ensure that this remains a robust revenue base for New Zealand.

The NRWT and/or AIL apply to direct and portfolio investors. International standard practice is to tax these different categories of investment quite differently. However, the details of international practice vary substantially across countries. New Zealand’s rules also treat direct and portfolio investors differently.

For direct equity investments (i.e., investments where an investor has an interest of 10 percent or more), company tax is the most important impost. NRWT is not levied on fully imputed dividends and there is also relief from NRWT on unimputed dividends under some Double Tax Agreements (DTAs). Where direct investors supply debt capital, NRWT is levied on interest payments, in keeping with the practice in many OECD countries.

For foreign portfolio (FPI) equity investments (i.e., investments undertaken by foreign investors who do not have a direct interest), company tax is once again the most important tax impost. NRWT has been maintained on dividends, but considerable relief has been granted through the foreign investor tax credit (FITC) and supplementary dividend payment system. NRWT on portfolio interest (i.e., interest paid to foreign parties who do not have a direct equity interest) is often reduced through the AIL regime.

The impact of taxation on foreign direct investment

For New Zealand, FDI is the main form of inbound equity investment. As at December 2015 the stock of foreign direct equity investment was $66.4 billion and the stock of FPI equity investment was $33.5 billion.[4]

Company tax collected from companies that are 50 percent or more owned by non-residents was approximately $3,420m (out of total company tax collections of $10,133m) and around $130m was collected in NRWT in 2014. The company tax number will be an over-estimate of taxes on inbound FDI as it includes tax paid on behalf of domestic and non-resident portfolio investors in these companies.

Taxing an activity reduces its attractiveness. Accordingly, taxing the income from FDI will undoubtedly reduce the incentive for non-residents to invest in New Zealand. Or, to put it another way, tax will drive up the pre-tax cost of capital (i.e., the minimum pre-tax rate of return that investments need to generate in order to be attractive on an after-tax basis). But this is only part of the story as the next section will discuss.

There is a reasonable degree of consensus in the literature that FDI is normally highly sensitive to the company tax rate and there is some evidence that this sensitivity has increased over time. However, there are no studies we are aware of on the sensitivity of FDI to the company tax rate in New Zealand. The sensitivity of FDI to domestic company taxes is likely to differ markedly across countries. One might imagine that FDI into a small landlocked country in Europe might be very responsive to taxation. Whether one sets up a factory in Austria or Germany close to the border, much the same market can be supplied from the factory. As a result, Austria is likely to find that the taxes it imposes are an important factor influencing where the factory is located and hence affecting the level of FDI.

For an island nation like New Zealand, which is a very long way from the rest of the world, much FDI may be associated with supplying goods and services to domestic markets. It will often be hard to do this without establishing a base in New Zealand. In this case, tax is much less likely to play a critical factor in investment decisions.

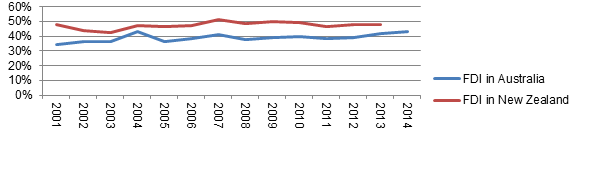

An international study by de Mooij and Ederveen (2005) suggested that, while there was considerable variability across studies, on average over a wide set of studies every percentage point cut in the company tax rate was estimated to increase FDI by about 3.72%.[5] If New Zealand were an “average country” this would suggest that its two reductions in the company rate (from 33% to 30% in 1 April 2008 and from 30% to 28% in 1 April 2011) should in aggregate have boosted FDI by about 18.6% (or from about 50% of GDP to more than 59% of GDP). However, there has been no surge in FDI into New Zealand over this period. Nor has there been an increase relative to Australia, whose tax rate remained constant over this period. (The small company tax rate in Australia has since been reduced to 28.5% with effect from 1 July 2015.)

Obviously this is not a scientific statistical analysis. Other things were happening at the same time, such as the Global Financial Crisis and other tax changes (for example, New Zealand’s second company rate cut in 2011 was accompanied by tighter thin capitalisation provisions and a tightening of depreciation rules). Nonetheless, it is a cautionary tale for those who would suggest that manipulating tax rates is a magic bullet for promoting FDI that can overcome other more fundamental determinants of inbound investment. More targeted, smaller changes are likely to have even less effect than a rate change, positive or negative.

These changes in the level of FDI are shown in the following graph, which measures FDI as a percentage of GDP in New Zealand and Australia over the period 2001 to 2014.

Figure 1: Stock of FDI as percentage of GDP

The company tax

A standard model for analysing the appropriate level of taxation on foreign investment looks at a small open economy (SOE), (New Zealand would certainly qualify), importing a single type of capital. New Zealand is an SOE and under the standard SOE assumption this means that New Zealand faces a perfectly elastic supply of capital so it can import as much capital as it wants without affecting the returns that foreigners demand (net of any New Zealand taxes) for supplying their capital to New Zealand. If there are no economic rents, it gives a clear result. Except to the extent that taxes imposed in the SOE are creditable abroad, there should be no taxes imposed on inbound investment. Any tax imposed will be passed forward onto other factors of production such as land and labour (or at least relatively immobile labour), but in a manner which is less efficient than taxing those factors directly. As company tax is the major tax on inbound investment, this would be an argument for eliminating company tax, at least on inbound investment.

If there is a single form of foreign capital (equity) and New Zealand can import as much of it as it wishes at a fixed return of, say, 4%, we have a simple story. Levy no tax and investments need to earn 4% to be marginally profitable. Levy a 20% company rate and investments need to generate 5%. Levy a 33.33% company rate and investments need to generate 6%. Thus, company tax rate drives up the pre-tax cost of capital. In this standard model with no economic rents, all investments are assumed to generate exactly the same rates of return, so the tax drives up the pre-tax rate of return on all investments.

In this very simple story, the after-tax cost of capital to New Zealand (i.e., the rate of return after subtracting New Zealand taxes) is always 4%. Inefficiency arises because economic investments (those earning between 4% and 6%) are not being undertaken. This lowers income of New Zealand fixed factors in a less efficient way than if they were taxed directly.

The cost of the tax is not borne by foreigners. Irrespective of the New Zealand company tax rate they always obtain 4% net of New Zealand taxes. The cost of the foregone investment is borne by New Zealand factors of production (typically land and relatively immobile labour). The under-investment that results from taxing foreign investment means that New Zealand factors of production are less productive and earn lower income. They could be made better off by eliminating the tax on foreign investment and taxing labour and land income directly.

Under this simplified analysis, taxation always distorts private decisions in ways that are inefficient from New Zealand’s point of view.

Despite this well-known analysis, New Zealand, like most other OECD countries, has chosen to impose a substantial tax on inbound capital. Why is this?

A key reason is the standard model is too simple to analyse many of the most important issues when setting taxes on inbound investment.

Also there is a question of where we would stop if we were to accept the zero tax proposition. New Zealand not only has very mobile capital inflows, it also has an extremely mobile labour force.[6] Exactly the same arguments that lead to a zero tax conclusion for taxes on income from inbound investment could be used to argue for a low or zero tax on workers with skills that are in high international demand if this makes them highly internationally mobile. Again, taxing the income of such workers would largely be borne by other factors of production such as land and less mobile labour but in a less efficient way than if they were taxed directly. Attempting to target personal income taxes according to the likely mobility of workers would be extremely divisive. New Zealand has a top marginal tax rate of 33%, which is relatively low by OECD standards. Arguably, keeping tax rates low across the board is a better approach than attempting to have low tax rates only on highly mobile workers. This is facilitated by maintaining a robust company tax.

The company rate New Zealand has set has involved a balancing of different issues. These are outlined below. Some push against cutting the company tax rate (or possibly even increasing the company rate) while others push in the direction of a lower company rate.

Location-specific economic rents

One reason pushing against cutting the company tax rate is that this would mean reducing taxes on location-specific economic rents. Economic rents are returns over and above those required for investment in New Zealand to take place. It is widely recognised that location-specific economic rents provide a justification for taxing inbound investments, even when the supply of foreign capital is perfectly elastic. Location-specific rents arise from factors that are linked to a location. Such factors could include resources, or access to particular markets that allow above normal profits to be earned. The rents can be subjected to tax since a portion of the rent would still accrue to the investor so that they could still earn more than their required rate of return even with the tax impost.

Even if companies are owned by domestic residents, there is a reason to tax these rents because doing so provides an efficient way of raising revenue. Tax revenue can be raised without distorting investment decisions. However, where companies are owned by non-residents there is a stronger reason still. A tax on these rents would be essentially borne by non-residents. This is less costly to New Zealand than if taxes are imposed on New Zealanders. Nevertheless, otherwise standard assumptions would still suggest exempting the normal rate of return on such investments from tax.

There are some alternatives to a standard company tax that have been proposed, such as an ACE (allowance for corporate equity) tax system, that allows a normal rate of return as a deduction on equity investments. An ACE company tax system is aimed at taxing economic rents as a residual. However, it does not make much sense to use an ACE for taxing companies owned by New Zealanders when individuals are taxed on their capital as well as labour income. An ACE would allow an individual to put savings into a company and for the company to earn tax-free interest on these savings. This does not seem sensible if we are attempting to tax individuals on their interest income. An ACE is also likely, in practice, to lead to lower taxes on sunk investments because restricting an ACE to only new investment is unlikely to be practicable. In New Zealand, an important source of rents is land rents, which are likely to be largely capitalised into prices. If there were no tax on “the normal return”, this could lead to forgiving tax on land rents. This would lead to a windfall benefit to those who are currently earning taxable income from land and other sunk investments, and create a major hole in the tax base. This is a big issue. Replacement taxes are likely to be more distortionary. Finally, bold new initiatives like an ACE can open up international avoidance concerns. An ACE and other alternative approaches were examined and rejected in our Savings and Investment Taxation Review.[7]

Sunk investment

A second reason pushing against cutting the company tax rate is that this would mean reducing tax on sunk investments and land, and provide windfall gains to existing owners of firms with these assets where the firms had undertaken the investment in the expectation that future returns would be taxed. As discussed above in the context of an ACE, replacing this revenue source is likely to involve distorting taxes, which could be more costly to New Zealand than the taxes that have been replaced.

Foreign tax credits available abroad

A conventional reason against cutting the company tax rate has been the availability of foreign tax credits abroad. If foreign governments provide credits for New Zealand taxes, cutting the company tax rate would mean forgoing revenue that is generally agreed to be New Zealand’s right to tax. At the same time it would be likely to increase tax revenue abroad rather than making inbound investment more attractive. However, over half of FDI into New Zealand (approximately 52 percent) is from Australia, which exempts foreign active income. Moreover, countries have been moving away from tax systems that allow credits for underlying company tax, and now the only major country allowing credits for underlying company tax is the United States. Thus, this argument has grown weaker over time. On the other hand, creditability continues to be an issue for other taxes such as NRWT as will be discussed later.

Less than perfectly elastic supply of inbound capital

While capital imported into New Zealand is highly elastic it is likely to be less than perfectly elastic. This may possibly mean that some of the burden of the company tax falls on non-resident investors and pushes against the idea that lowering the company tax rate as much as possible is necessarily desirable on economic efficiency grounds.

Once we start to allow for more than one form of capital, the perfect elasticity assumption seems to be undermined in a quite fundamental way. If there were more than one form of capital that were supplied perfectly elastically, we would only get the two forms of capital supplied simultaneously as a knife-edge solution when tax rates are set exactly right. Tiny changes would eliminate one or more of the forms of capital being supplied (for example, direct equity, portfolio equity or portfolio debt). This just does not seem credible. A real challenge to the simple model provided earlier of New Zealand facing a perfectly elastic inflow of capital is that this breaks down once we start to allow for multiple types of capital inflows.

In practice, different capital flows may be more or less elastic and a fuller economic model would take this into account.

Relationship to personal income tax

As company tax rates move downwards in other jurisdictions, New Zealand is open to the criticism that when we apply BBLR to company taxation we emphasise BB rather than LR. We are willing to have a higher than average company rate as part of a package, including imputation and reasonable alignment of company and top personal rates, which achieves a BBLR approach more generally for taxing income of New Zealand individuals earned through companies.

While the company tax is a final tax on income from inbound direct investment from New Zealand’s point of view, in the domestic context it is better viewed as a pre-payment of tax payable on the income accruing to shareholders. The imputation system then links company taxation to shareholder taxation to ensure that only one level of tax is paid, at the shareholder’s tax rate, on the underlying company income.

Keeping the company tax rate at or near the level of the tax rates applying to individuals and trusts plays a significant role in ensuring the integrity of the tax system in a simple manner. New Zealand suffered a salutary lesson in allowing misalignment of these rates to persist over the 1999 to 2010 period. Significant tax planning occurred. The 2010 Budget substantially fixed this misalignment. By aligning the trustee and top personal marginal tax rates, and keeping the company tax rate reasonably close (backed up by imputation), the incentive for tax planning has been reduced. If company tax rates were to be reduced, it would most likely be necessary to introduce measures to prop up the integrity of the personal tax system. This would undoubtedly add considerable complexity to the tax system, especially for SMEs.

Transfer pricing and tax base erosion

On the other hand, there are other arguments which push in the direction of a lower company tax rate. For example, there is evidence that higher company tax rates provide an incentive for multinational companies to undertake tax planning to shift profits from higher tax rate jurisdictions. This lowers their taxable revenue and national income. A recent study by Heckemeyer and Overesch (2013)[8] provides a consensus estimate from the literature. This suggests that a 1 percentage point cut in the company tax rate in a subsidiary relative to that of the parent company boosts the income it reports by 0.8%.

This is an “on average” result and the exact effects are likely to differ across countries. New Zealand has enacted a series of rules, such as transfer pricing, thin capitalisation, CFC rules and anti-arbitrage provisions to attempt to buttress the system against such techniques. We consider that these are likely to be relatively robust compared with the rules in many other countries, which is likely to mean that New Zealand is less susceptible to profit streaming than many other countries. Also, New Zealand’s full imputation scheme reduces the incentive for profits to be streamed away from New Zealand when New Zealand firms invest abroad but there is no hard data on any of this.

Nevertheless, as company tax rates in other jurisdictions fall, the incentives for international profit shifting increases. This can be an important consideration in evaluating New Zealand’s tax rate.

Distortions

New Zealand’s BBLR tax system attempts to tax different types of corporate investment as consistently and neutrally as possible. This is a cornerstone of New Zealand tax policy and helps ensure that investment distortions are minimised. However, some distortions in the measurement of economic income inevitably remain. Keeping the tax rate as low as possible reduces the size of these distortions.

The rate of company tax

The company tax is levied on both foreign direct and FPI equity investment. These balancing considerations apply for both types of inbound equity investment.

At the time of New Zealand’s Savings and Investment Taxation Review in 2012 officials looked at whether there was a pressing case for further cuts in the company tax rate. We concluded that once we took account of the fact that a significant part of the benefits of further company rate cuts may accrue to non-residents while the costs of replacement taxes are likely to fall on New Zealanders, further cuts in the company tax rate were not a priority at that time and had the potential to make New Zealand as a whole worse off. Further cuts to personal tax rates were judged to be a higher priority.

Nothing has changed since 2012 that would lead officials to reverse their conclusions on this issue. At the same time it should be acknowledged that this is a judgement call. For a discussion of pros and cons of a company tax rate cut in Canada, which comes out as broadly supportive of a cut in combined federal and provincial statutory rates to around 25%, see Zodrow (2008).[9]

International tax settings are dynamic. In particular, Australia has signalled its intention to cut its company tax rate in the future although, at least for larger businesses, these cuts are some time in the future. The intention is to cut the company rate first for small companies to 27.5% in 2016/17, and follow this up with a cut for larger companies to 27.5% in 2023/24, with a further cut in the company tax rate to 25% for all companies in 2026/27. The Australian projected tax cuts for larger companies are a long way off but as other countries cut their company rates, transfer pricing concerns place additional pressure on a small open economy such as New Zealand to do likewise. Thus, New Zealand’s company tax rate is something which needs to be kept under review.

Non-resident withholding tax (NRWT) on interest on related-party debt

NRWT sits rather uncomfortably in an economic discussion of best-practice taxation. To some extent, NRWT has traditionally been bolted onto the tax system in a rather ad hoc manner. One virtue is its simplicity. On the other hand, its blunt nature raises the possibility of introducing unintended distortions in investment decisions and business arrangements.

NRWT has traditionally served a number of functions:

- NRWT allows source countries to collect tax on some forms of income derived locally by non-residents. However, DTAs limit the rights of source-countries to impose tax on this income. As such, they determine the sharing of the international tax base between residence and source countries. Setting their rates is less a matter of determining efficient tax policy than a negotiation between states to divvy up taxing rights. In this case, the application of residence-country taxation is an important part of the story.

- In some cases, NRWT is a proxy tax on revenue streams that is intended to avoid the complexity of a net basis tax calculation.

- When NRWT is applied to payments that give rise to deductions against the income tax base, it can provide a backstop to the income tax, thus minimising the potential for base erosion by such payments.

In the case of interest payments to related parties, levying NRWT is the international norm. The OECD model tax treaty restricts NRWT on interest to 10% but allows a credit for this in residence countries. This is an attempt to share tax on interest paid across borders in an equitable way.

Interest is generally deductible in New Zealand and taxable in the residence country of the parent company with a foreign tax credit for any NRWT paid to New Zealand. There are a number of situations that are relevant for the taxation of the interest.

Foreign tax credits available to parent

When foreign tax credits are available in the residence country, cutting the NRWT would simply transfer our negotiated share of the tax to the residence country with no effect on the return to the investor and accordingly no effect on the cost of capital to New Zealand. This effect is illustrated in Table 1. It would be a pure welfare loss to New Zealand with no increased incentive to invest for the investor. New Zealand’s loss of tax revenue would be a loss of national income. It is this model which undoubtedly underlies the international norm of applying NRWT on related-party interest.

Table 1: Effect of NRWT on share of tax

| With NRWT | Without NRWT | |

|---|---|---|

| New Zealand | ||

| Interest paid | 100 | 100 |

| NRWT | 10 | 0 |

| Residence country | ||

| Interest received | 100 | 100 |

| Tax before credit | 28 | 28 |

| Foreign tax credit | 10 | 0 |

| Tax after credit | 18 | 28 |

| Total tax | 28 | 28 |

At times a parent may be entitled to foreign tax credits but these may be restricted. This may be because NRWT is levied on a gross interest payment but when a foreign parent is borrowing and then lending to its subsidiary, the parent’s foreign profits will only reflect an interest margin. It is quite possible for a 10% tax on gross interest received by the parent to be greater than the parent’s company tax liability on the profits. In this case NRWT is likely to be only partially creditable. This is likely to increase the pre-tax cost of capital. But it is also likely to encourage foreign parents to finance their domestic subsidiaries with equity rather than debt, which could tend to increase New Zealand’s national income for reasons discussed in the section on “Debt and equity advanced by a foreign parent and thin capitalisation provisions”.

Tax-exempt parent

NRWT will not be creditable if the foreign parent is a non-taxpayer. Some countries exempt certain non-taxpayers from their NRWT. New Zealand’s position has been to offer exemption only in limited circumstances.

There are good grounds for this policy. It is based on the idea that what happens in the residence country should not deter New Zealand from collecting its share of tax on income earned within its borders. To offer an exemption from NRWT would raise the possibility that an exempt taxpayer could substitute for a taxable investor, lowering New Zealand’s tax revenues without adding to investment in New Zealand. Table 2 demonstrates that a substitution costs New Zealand tax revenue and national income. The table assumes that the investment is just as productive in the hands of the subsidiary of the exempt parent as it was in the hands of the subsidiary of the taxable parent, earning $100 of revenue in either case. Less tax in New Zealand means that the foreign owner earns more and New Zealand’s national income falls.

Table 2: Effect of NRWT exemption for tax-exempt parent

| Taxable company | Tax exempt | |

|---|---|---|

| Revenue | 100 | 100 |

| Interest expense | 100 | 100 |

| NRWT | 10 | 0 |

| Benefit to New Zealand (contribution to NZ national income) | 10 | 0 |

| Return to parent | 90 | 100 |

Debt and equity advanced by a foreign parent and thin capitalisation provisions

The single most important tax base issue in determining New Zealand’s share of the taxes payable on income earned on FDI is the method of financing employed by the parent company of the New Zealand operations. In particular, is the New Zealand subsidiary[10] financed by debt or equity from the parent?

The distinction between debt and equity is largely arbitrary in related-party situations. The overall risk to the parent company is not generally affected by choices between these two methods of financing the operation of subsidiaries. The arbitrary nature of the distinction means that in the absence of any restrictions a New Zealand subsidiary could be financed almost exclusively with debt which might lead to interest deductions offsetting most or all income otherwise taxable in New Zealand.

The amount of tax payable to New Zealand on the investment is substantially affected by the choice. Investments funded by equity are subject to full taxation at the 28% company tax rate on the income generated by their New Zealand operations. On the other hand, for investment funded by debt, the interest paid is deductible against the income tax base in New Zealand. Accordingly, the New Zealand tax paid on the underlying income is the NRWT at a rate of 10% or 15%, depending upon whether the residence country of the parent is a treaty country or not.

Thin capitalisation rules can play an important role in restricting interest deductions so that they do not unduly erode New Zealand’s share of tax.

Unlike in many jurisdictions, New Zealand’s thin capitalisation rules apply to unrelated party debt, as well as related party debt. Rather than a parent lending directly to its New Zealand subsidiary, it could arrange for the subsidiary to hold much higher third-party debt than the parent. This can be a close substitute for direct lending by a foreign parent. Accordingly, the rules respond to concerns about third-party borrowing being done through New Zealand in a manner that erodes the tax base. Australia’s thin capitalisation rules also apply to both related and unrelated-party debt. Thin capitalisation rules limit base-erosion by a variety of BEPS schemes that rely on increasing interest deductions.

While the underlying policy framework for thin capitalisation is an apportionment of debt among countries, a safe-harbour ratio of debt to assets, below which interest is not restricted, simplifies compliance with the rules. The safe harbour has relatively recently been changed from 75% to 60%. This change has been paralleled in a number of other jurisdictions, notably Australia, which has a thin capitalisation framework similar to New Zealand’s.

Thin capitalisation rules on inbound investment could potentially increase both tax revenue and national income through the replacement of debt with equity. At the same time, they could discourage investments that would otherwise be economic by raising taxes on such investment. These are trade-offs that need to be thought through.

To see these as simply as possible, initially suppose that $1,000 could be invested into New Zealand and that this generates revenue of $100 per annum. The capital can be advanced as debt or equity by a foreign direct owner of the New Zealand firm, which is exempt in its home country on dividends from its New Zealand subsidiary, but taxed on any interest receipts. Also suppose that the foreign owner is resident in a country which, like New Zealand, has a 28% company tax rate. Suppose that the owner requires a 10% pre-tax return or 7.2% post-tax return on its funds. For simplicity, we ignore any withholding taxes.

This investment would be a break-even or marginal investment whether the parent finances it with debt or equity. Cashflows in the two cases are outlined in Table 3.

Table 3: Effect of debt and equity on country of taxation

| Debt financed | Equity financed | ||

|---|---|---|---|

| New Zealand company level | |||

| Revenue | 100 | Revenue | 100 |

| Tax | 0 | Tax | 28 |

| Interest payment | 100 | Dividend | 72 |

| Benefit to New Zealand [11] | 0 | Benefit to New Zealand | 28 |

| Foreign company | |||

| Interest income | 100 | Dividend income | 72 |

| Tax | 28 | Tax | 0 |

| After-tax cashflow | 72 | After-tax cashflow | 72 |

If the investment were fully debt financed, New Zealand would receive no net tax revenue from the investment. If, on the other hand, the investment were fully equity financed, New Zealand would receive net tax revenue of $28 and its national income would be $28 higher. In both cases the company receives the same after-tax income of $72. An important implication of the example is that the total tax burden on the investor does not change as the debt-to-assets ratio into New Zealand changes – only the sharing of the tax revenues between New Zealand and the residence country changes. In this case thin capitalisation rules do not decrease the pre-tax cost of capital or the incentive to invest in New Zealand.

Of course there are situations when this is not true. For example, if the foreign country had a lower company tax rate than New Zealand, the foreign parent would prefer to debt-finance its New Zealand subsidiary and tighter thin capitalisation rules would lead to an increase in the effective tax rate on inbound investment and an increase in the pre-tax cost of capital for that investor. Also, some countries have weak CFC rules that can allow interest income to accumulate in tax havens without any tax. This means that interest expense that is deductible in New Zealand may not end up being taxed anywhere in the world.

As was discussed at the time of the Tax Working Group,[12] choosing thin capitalisation thresholds will involve trade-offs between the potential effect on the pre-tax cost of capital and level of investment on the one hand and the benefits to New Zealand arising from having taxes paid in New Zealand on the other.

Moreover, there are other issues as well that may be important. An important consideration when the thin capitalisation safe harbour was reduced from 75% to 60% was that 75% was an extremely high level of debt that would not be seen in arms’ length situations. Thus, the former safe harbour was seen as allowing an unreasonable stacking of debt into New Zealand. New Zealand’s actions here can be seen as an early response to concerns about BEPS.

Some have also argued that there can be a competitive distortion if multinational enterprises (especially those based in countries with weak CFC rules) can out-compete domestic firms because of differences in opportunities to avoid taxes. This is complex to analyse because there are many different factors (including New Zealand’s full imputation system and its FITC regime), which can affect any such competitive distortions. But there were no doubt some instances when New Zealand’s former high safe harbour may have made it more attractive for a non-resident shareholder to invest into New Zealand via a foreign company rather than through a New Zealand company. These incentives would have been reduced by the tightening of the safe harbour.

It should be acknowledged that the thin capitalisation safe harbour is ultimately a judgement call. There is no hard evidence which would allow us to determine an “optimal” safe harbour ratio.

Deviations from normal rules, marginal investors and welfare implications

At times, as a result of either some intended reason or perhaps an inadvertent loophole in the tax system, there may be deviations from normal tax rules in certain cases. A deviation from normal taxation could arise when we have a general tax on inbound investment but some investors are able to reduce New Zealand tax payable on particular transactions.

If capital were supplied perfectly elastically, the economic effects of the deviation would depend on whether the tax reduction is sufficiently broad to significantly change the aggregate amount of investment in New Zealand or the pre-tax rates of return in the economy. That is, the effects will depend on the identity of the marginal investor into the economy.

Assume, as earlier, that most foreign investors require a 4% rate of return net of any New Zealand taxes. We have a general tax rate of 33.33% and a marginal pre-tax rate of return of 6% is needed for a fully taxable non-resident to earn their required 4% return. On this investment, non-residents are receiving 4%, so New Zealand is earning 2%.

First, suppose an exception from the general treatment is used by a narrow group of non-resident investors, which allows them to pay no tax. If these investors can compete away assets from the fully taxed investors and use them just as productively, the investments would still be getting a return of 6% but now the non-resident captures the entire 6%. New Zealand has lost the 2% of tax. This is a loss of both tax and national income.

Because the group that cannot benefit from the exception is large, and that at the end of the day it will always be an important investor into New Zealand, it will be the marginal investor under standard assumptions. Under standard assumptions, this group will be the marginal investor. As noted, this group of investors requires a pre-tax rate of return of 6% for investing into New Zealand so that the pre-tax rate of return will not be bid down below this rate by the investors enjoying the deviation from normal taxation. In this case the substitution discussed above is the only thing that happens. The deviation from normal rules does not affect the general pre-tax cost of capital or the level of investment in the economy. However, the cost of funds to New Zealand net of any New Zealand tax (or the post-tax cost of capital) has increased from 4% to 6% for those investors who are able to benefit from the deviation. The deviation is costly to New Zealand. In this case, a provision that eliminates the deviation would not affect New Zealand’s pre-tax cost of capital and would increase its national welfare.

A reduction that could only be exploited by certain taxpayers would distort the allocation of investment by favouring such taxpayers. In general, there are strong grounds for keeping tax rules on inbound investors as neutral as possible. This is an important reason for amending provisions in the tax system that allow certain taxpayers to escape tax in ways that are not intended. In other words, neutrality and national welfare can be enhanced through base-maintenance measures. There should be a high burden of proof before moving away from general BBLR tax principles.

Another possibility is that the deviation has sufficiently widespread effects that it drives down the pre-tax cost of capital in the economy and increases investment markedly. If the inflow of capital into the economy really were perfectly elastic, this would render investment into New Zealand uneconomic for those investors who remain fully taxed. Those who can use the concession would become the marginal investors.

A broader tax reduction would raise many of the considerations discussed above in setting the general company tax on inbound investment, and the discussion of those measures should be seen in that broader light. To the extent that taxing inbound investment was seen as appropriate generally, there would be little reason to allow that tax to be circumvented. Moreover, allowing a deviation for some groups but not others is likely to be considered unfair.

In practice, the supply of capital from different foreign investors is likely to be less than perfectly elastic. Different investors will have different expertise and expectations and it is most unlikely that there is a single group of marginal investors. But if a deviation allows a small group of preferred investors to out-compete a large group of investors who do not benefit from the deviation, it is very likely that the deviation will have a direct effect in reducing national income.

BEPS

BEPS arises when multinational companies arrange their affairs so that no or minimal tax is paid anywhere on their income. This can occur by shifting profits to low-tax countries or by exploiting arbitrage opportunities between countries. An example would be using an instrument which gives rise to deductible interest in New Zealand, but tax-free dividends in the resident country. One possible way of examining the costs and benefits of changes here is to take other countries’ tax rules as fixed and to ask what is in New Zealand’s best interest given these overseas rules. In this case, whether tax changes are good or bad for New Zealand is not clear cut and depends on the tax outcomes in the absence of the BEPS arrangement. If, in the absence of the BEPS arrangement there would be no tax in New Zealand, then the BEPS arrangement would only avoid taxation by the resident country. There would be no incremental cost to New Zealand. On the other hand, the BEPS arrangement could result in less tax being paid in New Zealand. These situations are analysed in turn.

Resident country tax avoided

If New Zealand would not tax the income in the absence of the BEPS arrangement, an arrangement that avoids residence-country taxation would make New Zealand better off. In this case, for a given investment with a given pre-tax rate of return, the return to the investor increases and New Zealand continues to earn the same level of tax revenues. Reduced taxes overseas will lower the after-tax cost of capital to New Zealand and provide an increased incentive to invest in New Zealand. In this case, if one focuses solely on what is best for New Zealand, allowing the BEPS strategy would appear to be beneficial to New Zealand.

New Zealand tax avoided

On the other hand, consider a situation where the BEPS strategy results in lower taxes in New Zealand, but no offsetting increase in tax in the residence jurisdiction. NRWT is also assumed to be avoided.

In effect the investment is exempt from tax. If the investor is replacing a fully taxable investor, (which could have been themselves before the arrangement), there would be a clear loss of welfare to New Zealand. The BEPS arrangement is likely to lead to a loss of tax revenue and national income to New Zealand.

In many cases BEPS issues arise from arbitrage across countries’ differing definitions of debt and equity. Arbitrage can occur if a payment is treated as a deductible interest on debt in New Zealand and as a non-taxable dividend in the residence country.

An important consideration is whether this arbitrage is likely to be leading to a reduction in taxes in the country where the foreign investors reside or in New Zealand. If taxpayers were generally at their thin capitalisation thresholds, then it is likely that resident taxation is being avoided on the margin. This is likely since interest deductions would already have been maximised in New Zealand, and the BEPS arrangement would not result in a reduction in taxes paid New Zealand. It can be argued that New Zealand would benefit from the scheme in such situations. However, many non-resident-owned companies are not at their thin capitalisation thresholds. In that case, allowing the schemes would risk reducing New Zealand’s tax base and national income if the taxpayer were induced to increase their level of deductible interest expenses in New Zealand as a result of the arbitrage. In that case the BEPS arrangement appears likely to have a direct cost to New Zealand.

Broader context

The considerations discussed above have looked at New Zealand’s interest in isolation, taking other countries’ tax rules as fixed. There are more general arguments in favour of joining a multilateral effort to remove arbitrage possibilities (which are at the heart of many BEPS issues). When companies engage in BEPS, the result is that no tax is paid anywhere on a portion of income. This clearly leads to an inefficient allocation of investment internationally as cross-border investments are subsidised relative to domestic investments. Eliminating this misallocation would increase worldwide efficiency, leading to higher worldwide incomes. The best approach for New Zealand may be to co-operate with other countries in eliminating this worldwide efficiency in the hope of gaining its share of this extra worldwide income.

Double non-taxation reduces company taxes worldwide. While there may be arguments that in certain circumstances the cost falls on other countries, it would be naïve to suggest that the cost never falls on New Zealand. Experience suggests that once taxation is eliminated in the residence country, source country taxation is placed at risk. For example, the BEPS-induced decline in US taxation of US residents’ foreign-sourced income is often cited as a major reason for the increased focus on reducing source-country taxation by US multinationals. In that case, a general move to eliminate BEPS possibilities would make tax collections in all countries, including New Zealand, more secure and less vulnerable to unexpected tax planning.

Moreover, quite random reductions in tax, depending upon the opportunism of taxpayers, are likely to distort the allocation of investment in New Zealand and lead to complex arrangements that are themselves a source of inefficiency. An important priority for the Government is considering rules to address BEPS. This includes two measures that are on the current Tax Policy Work Programme, viz., rules to address hybrid mismatches and the possibility of tighter interest limitation provisions.

There is a broad public concern that BEPS is unfair. Large companies escaping tax while earning substantial profits in a country has been the subject of considerable public controversy. Overall there are strong arguments for considering initiatives in this area. However, when considering initiatives we obviously should not lose sight of the importance of keeping New Zealand an attractive place to base a business and invest. Cost of capital issues will be an important consideration, especially in the case of interest limitation changes, where (depending on options chosen) changes are likely to have the biggest effects on the cost of capital.

New Zealand has been a supporter and significant contributor to the BEPS initiative. However, the foregoing comments should not be seen as supporting adoption for New Zealand of any particular BEPS proposal emanating from the OECD. Each initiative needs to be looked at critically from New Zealand’s point of view. Public consultations are necessary and any proposals would be subject to the full Generic Tax Policy Process (GTPP).

Unrelated-party debt and NRWT/AIL

An important tax issue is the treatment of interest on debt between unrelated parties that is borrowed from abroad. Such interest is subject to the NRWT and AIL regimes. While there is some overlap with the analysis with respect to FDI, there are substantial institutional and economic differences, which can lead to different analysis and conclusions.

New Zealand provides borrowers from unrelated lenders with the option of paying either NRWT (which under New Zealand’s DTAs is normally taxed at 10%) or AIL, which is taxed at 2%. If lenders are able to claim full foreign tax credits (FTC) in their residence countries for New Zealand taxes, they would prefer the 10% NRWT. But if New Zealand taxes are not creditable, the 2% AIL will be preferred.

Thus, New Zealand’s tax rules are likely to result in NRWT being chosen when lenders are able to claim FTC, and AIL being chosen in other cases. This has the potential to collect some NRWT without pushing up interest rates very much in New Zealand.

Table 4 records revenue figures for NRWT on interest and AIL for the year to March 2014. Total NRWT on interest was $135m of which $42m was paid by banks leaving $93m of other NRWT on interest being paid. Much of the $42m of NRWT paid by the banks may be on interest that foreign residents earn on New Zealand bank deposits where an alternative would have been to pay AIL. In addition, perhaps another $8m of the $93m is likely to be borrowing from third parties where the AIL option was available. The rest of NRWT appears likely to be raised on related-party lending (where NRWT is required). AIL (excluding amounts paid by the Government) amounted to $47m.

Table 4: Revenue figures

| NZ $million | |

|---|---|

| Total NRWT on interest 2014 | 135 |

| NRWT on interest paid by banks (presumably mainly to unrelated-party lenders) | 42 |

| AIL (excluding that paid by Government) | 47 |

New Zealand is the only country that provides the AIL option. Many other countries exempt interest on certain loans. Common examples are exemptions for interest on borrowing from foreign banks and from foreign superannuation funds and/or foreign sovereign wealth funds.

If NRWT could be levied without any change in domestic interest rates, there would be no reason for other countries to have provided this exemption or for New Zealand to have provided an AIL option. Under international conventions, source countries have a right to tax this income and this could be done without affecting the rates of interest that domestic borrowers pay. Indeed the NRWT collected would make the borrowing country better off.

To see this, suppose that there is a world interest rate of 5.0% and third-party debt capital is provided perfectly elastically at this price. Thus, a small open borrowing country can obtain as much in the way of borrowed funds as it wants at this interest rate.

In the absence of any taxes in the borrowing country, the domestic interest rate would be 5.0%. No borrower would be willing to pay a higher interest rate and competition between domestic borrowers and/or opportunities to lend abroad will mean that no lender need accept an interest rate less than 5%. (In practice, costs of financial intermediation are likely to drive a gap between borrowing and lending rates but, for simplicity, we ignore this issue.) If NRWT could be levied without affecting the interest rate, this would mean that the domestic interest rate would remain 5.0% but now the cost of borrowing to the borrowing country as a whole would fall to 4.5% because NRWT of 0.5% would be levied. This NRWT would be both a source of tax revenue and a source of international income to the borrowing country.

It should be noted that if this really were the world we are in, New Zealand’s AIL option would be a bad idea. Any borrowing from abroad where AIL is levied would be displacing borrowed funds that only cost New Zealand as a whole 4.5%. This would be increasing the cost of borrowing to New Zealand.

However, the typical motivation for the exemption that other countries provide for borrowing from certain lenders is that such lenders are unlikely to be able to benefit from FTC for the NRWT in their residence countries. In that case there is a concern that the NRWT would be passed forward and result in higher borrowing costs in the domestic economy. Providing targeted exemptions can be seen as a way of attempting to ensure that NRWT does not lead to a significant increase in domestic interest rates. As such it can be seen as an alternative way of accomplishing the goals of AIL.

There is some evidence that foreign lenders who cannot use credits for NRWT are the marginal foreign lenders whose demands end up setting domestic interest rates.[13]

Some countries have broader exemptions on unrelated-party debt. These exemptions respond to concerns that applying withholding taxes can raise the cost of borrowing generally in the economy and so act as a type of tariff on imported portfolio debt, raising the pre-tax cost of capital. Nevertheless, a general exemption can mean the borrowing country will lose revenue from infra-marginal lenders who can use FTC. Accordingly a general exemption would appear to be a second-best strategy, compared with an approach such as AIL, that tries to target the reduction in NRWT to lenders that cannot use FTC in the residence country.

Pros and cons of AIL/NRWT option compared with targeted exemption

An obvious question is whether New Zealand’s AIL/NRWT option is likely to be preferable to the targeted exemptions from NRWT provided in other countries for interest paid to foreign lenders.

New Zealand’s AIL/NRWT option does mean that there will be a small AIL tax impost on interest paid to marginal lenders. This is likely to push up domestic interest rates very slightly (for example, from 5.0% to 5.1%). This is likely to have some effect on pushing up the pre-tax cost of capital in New Zealand although this effect is likely to be tiny.

At the same time AIL does raise some revenue to help finance government spending. It also helps support NRWT collections by restricting exemptions from NRWT to only those foreign lenders who cannot absorb an NRWT liability.

Overall we consider that New Zealand’s AIL/NRWT option continues to be a reasonable way of targeting the NRWT exemption.

There are some other considerations which add to the case for continuing with the AIL/NRWT option.

First, there is currently a significant tax bias favouring imports of foreign third-party debt capital ahead of imports of either FDI or FPI equity. This is because interest payments are deductible whereas dividend payments to foreigners are not. A 2% AIL impost offsets this bias, albeit only very slightly.

Secondly, the discussion above has assumed that small open economies such as New Zealand face a completely fixed world interest rate. While New Zealand firms borrowing in foreign currencies are unlikely to pay much higher interest rates than their overseas counterparts, there is an ongoing concern that they face relatively high interest rates when borrowing in domestic currency. This may be because of a currency premium – perhaps brought about because of New Zealand’s large international indebtedness. In this situation measures which will tend to reduce international indebtedness such as the very small AIL impost may tend to be reducing the cost to New Zealand of its borrowings from abroad.

The bottom line is that we see no strong case for moving away from the current AIL/NRWT option in favour of a more conventional attempt to identify marginal third-party foreign lenders who are unlikely to be able to absorb NRWT, and provide exemptions to these lenders.

Implications of the branch loophole

Most major New Zealand banks are offshoots of foreign banks and have been able to sidestep paying AIL through the use of branch structures. More recently, widely held bonds issued by New Zealand companies have also been made exempt from AIL to overcome the competitive disadvantage that would otherwise be faced by these firms when issuing relative to borrowing from domestic banks.

It is not very clear how best to meld this possibility in with the rest of the analysis. Suppose that foreign lenders who cannot use foreign tax credits are the marginal lenders, and as a result of AIL, the domestic interest rate rises from 5.00% to 5.10%. The branch loophole would potentially allow domestic offshoots of foreign banks to undercut AIL by borrowing from abroad and lending at 5.00%. In this case, all of the benefit of the branch loophole would be passed forward to domestic borrowers and no AIL would be paid.

In practice, the offshoots of foreign banks who have been able to use branch structures and not pay AIL have been in competition with New Zealand-owned banks whose third-party loans are subject to AIL. Another possibility is that the loophole enhances the profits of these domestic banks with foreign parents. They can borrow from abroad at 5.00% and lend domestically at 5.10%. This would mean that the full benefit of the branch loophole accrues as additional profits of foreign-owned domestic banks and none would be passed forward to domestic borrowers. This would be costly to New Zealand. The loss of tax revenue to New Zealand would be a loss of national income.

The truth may lie somewhere between these extremes. However, even if the benefits of the branch structures were being fully passed on to New Zealand borrowers in the form of slightly lower interest rates, this would be undercutting the AIL collections and reducing the effectiveness of the AIL/NRWT mechanism.

This suggests the broader conclusion that there should either be an AIL/NRWT system or an exemption system, not a combination system of AIL/NRWT with exemptions. This has been addressed by the legislative changes proposed in the Taxation (Annual Rates for 2016–17, Closely Held Companies, and Remedial Matters) Bill, introduced in May 2016.

Summary of conclusions for unrelated-party lending from abroad

Our key findings for third-party debt financing are as follows:

- if the marginal lenders could use credits for NRWT, national income would be maximised by levying NRWT on interest payments abroad with no exemptions;

- however, it is likely in practice that the marginal lenders are FTC-constrained, and in this case under standard SOE assumptions, there is an argument for either exempting marginal lenders from NRWT or allowing an AIL/NRWT option;

- exempting marginal lenders from NRWT might be better than the current AIL/NRWT option if they could be accurately identified;

- overall, it is an open question as to how easy it is to identify marginal foreign lenders who are FTC constrained, which swings the balance back in favour of continuing with New Zealand’s AIL/NRWT option;

- there are some other considerations, including biases between foreign equity and foreign debt finance and domestic interest rates, which may increase with additional borrowing and may lend additional support for the AIL/NRWT option;

- provided that New Zealand continues with its AIL/NRWT option there is a good case for removing measures such as the branch loophole, which allows these taxes to be sidestepped.

Conclusions

The principal conclusions of this framework paper were outlined at the start.

There is no perfect way of taxing income arising on inbound investment. However, New Zealand’s current approach of levying company tax supported by NRWT on related-party debt, and an AIL/NRWT mechanism for third-party debt all make sense. So too do base-protection measures such as thin capitalisation and transfer pricing rules. At least in the near future we would expect any changes to be “at the margin” changes rather than a radical rewriting of the rules.

An important priority for the future will be to consider measures to address BEPS. This includes consideration of rules to address hybrid mismatches and the possibility of tighter interest limitation provisions. When addressing these issues the focus will be on doing what is in New Zealand’s best interest but, at times, this may mean co-operating with other countries to achieve a more efficient worldwide outcome and seeking to gain our share of a bigger worldwide pie.

There are important tradeoffs in all of this. We want a tax system that is fair and seen to be fair. We want a tax system which provides a robust revenue base to meet the Government’s spending priorities. We want the taxes to generally apply as neutrally and evenly as possible. At the same time it is essential that New Zealand maintains its position as a good place in which to base a business and invest. In considering policy changes it is important that they are subject to public consultation and full GTPP.

Appendix

Effective Tax Rates (ETRs) on inbound investment

The paper has outlined rules governing taxes on inbound investment and has also described some important changes in recent years. Changes in the future, and especially any changes affecting interest limitation provisions, could have impacts on effective tax rates and the cost of capital.

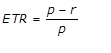

It is instructive to examine how ETRs have changed in the past. This also provides a way of examining how future changes may affect ETRs and the pre-tax cost of capital. The ETR is the proportion of the pre-tax rate of return that goes in taxes that impact on the returns the non-resident lenders or investors receive. We can write this as:

where p is the pre-tax rate of return on an investment and r is the return to foreign lenders or investors net of any New Zealand taxes or foreign credits for those taxes.

Table 5 illustrates how ETRs have changed over time. This updates calculations provided in the McLeod Review. ETRs will tend to drive up the pre-tax cost of capital.

Key changes have included a cut in the company tax rate from 33% to 30% in 2008 and a further cut in the company tax rate from 30% to 28% in 2011, which was accompanied by a tightening of the thin capitalisation safe harbour from 75% to 60%. Throughout the full period the AIL/NRWT option has been available for portfolio or third-party debt.

For portfolio debt we report maximum and minimum ETRs. The maximum ETR throughout the period occurs for lenders who choose the AIL option. This results in an ETR of 2% and drives up the pre-tax cost of capital by 2%. For example, if third-party lenders demanded an after-tax interest rate of 5%, the hurdle rate of return on an investment financed by this third-party debt would increase to approximately 5.1%. The minimum ETR is 0% for the period. This occurs for those who can absorb any credits for NRWT on interest where the NRWT option is chosen.

For portfolio equity investment, we also examine a maximum and a minimum tax rate. The maximum tax rate reflects the ETR for a FPI equity investor who is unable to claim credits for NRWT on dividends. In this case the effective tax rate is the company tax rate. This has fallen over time. The current ETR is 28%. Again taxes will tend to drive up the pre-tax cost of capital. If a foreign shareholder demanded a 5% after-tax return the company would now need to earn 6.94% because 6.94% x (1-0.28) = 5%.

For foreign shareholders who can utilise credits for NRWT, New Zealand’s NRWT will not impact on the ETR. The minimum ETR is the ETR for those who can utilise the credits. This minimum ETR has fallen from 21.2% to 15.3% as a result of the two cuts in the company tax rate.

For direct investment we ignore the possibility of company tax itself being creditable overseas as this is only likely to happen in a small minority of cases. We consider three possible cases. The first is where FDI is fully equity-financed. This is a reasonable approximation to what happens in a not insignificant number of cases. In this case the ETR is just the company tax rate. This has fallen over time. Secondly, we consider the maximum ETR for what we call a fully geared subsidiary. This is where the subsidiary is geared to the maximum safe harbour ratio so interest is fully deductible but only just and where the foreign owner of the subsidiary is unable to utilise any credits for NRWT. In this case the ETR is a weighted average of the ETR on equity (the company tax rate) and the ETR on debt (assumed to be 10%). For example, at a safe harbour which allows debt to be 75% of assets and a 33% company rate, the ETR would be 15.75%, (viz., 33% x 0.25 + 10% x 0.75). Finally, we examine a minimum ETR for a fully geared subsidiary. In this case it is assumed that the foreign owner of the subsidiary is able to absorb credits for NRWT on interest so the ETR only reflects tax on the equity component of income. For example, with a 33% company tax rate and 75% safe harbour, the ETR would be 8.25% (viz., 33% x 0.25).

Table 5: ETRs on inbound investment

| Pre-2008 | 2008–2010 | Post-2010 | |

|---|---|---|---|

| Portfolio debt | |||

| Maximum | 2.00 | 2.00 | 2.00 |

| Minimum | 0.00 | 0.00 | 0.00 |

| Portfolio equity | |||

| Maximum | 33.00 | 30.00 | 28.00 |

| Minimum | 21.28 | 17.65 | 15.29 |

| FDI | |||

| All equity | 33.00 | 30.00 | 28.00 |

| Maximum: fully geared | 15.75 | 15.00 | 17.20 |

| Minimum: fully geared | 8.25 | 7.50 | 11.20 |