Chapter 2 - The issue

2.1 This paper addresses an issue with the interaction between two sets of taxation rules. The issue is outlined below, and the associated consequences of it are also explained. The two sets of tax rules which underlie this issue are the loss grouping rules (found in subpart IC of the Income Tax Act 2007) and the imputation rules (found in subpart OB of the Income Tax Act 2007).

2.2 When a profit company and loss company engage in loss grouping less income tax is paid which results in the profit company receiving fewer imputation credits than it would have had it not engaged in loss grouping.

2.3 Having fewer imputation credits becomes an issue when that profit company later chooses to pay a dividend to its shareholders and the companies are not wholly owned. Unless the profit company is wholly owned by a corporate parent, the dividend will be taxable, and the imputation credits in the profit company’s imputation credit account will determine whether it is able to fully impute that dividend. In some cases, the profit company will have insufficient imputation credits to enable it to pay a fully imputed dividend. This results in a tax impost for the shareholder upon distribution of the loss-sheltered profits, effectively clawing back the benefit of the loss grouping.

2.4 This issues paper discusses whether this inability for non-wholly owned companies to fully impute dividends as a result of loss grouping is appropriate; and, if not, what a feasible solution may be.

2.5 A brief discussion of the policy underlying the two sets of tax rules is set out below.

Imputation rules

2.6 Imputation is a mechanism that allows the benefit of income tax paid at the company level to be passed through to shareholders by attaching imputation credits to dividends paid by the company to its shareholders. Resident recipients of imputation credits may use the credits to offset the amount of tax they would otherwise be liable to pay on those dividends.

2.7 Dividends paid between members of wholly owned corporate groups are generally exempt income (referred to as the inter-corporate dividend exemption).

Loss grouping rules

2.8 The Income Tax Act 2007 permits the sharing of losses between companies that are in the same “group of companies”, that is, they have at least 66 percent common ownership. If a company has made a loss it may elect to make the benefit of the loss available to another group company that is in profit.

2.9 Offsetting some or all of the loss against the net income of the profit company means the profit company will not be liable to pay as much tax as it would otherwise. However a consequence of paying less tax is that the company will generate fewer imputation credits than it otherwise would have.

2.10 Group companies can choose whether to effect the loss offset by way of a subvention payment, or simply by electing to offset the amount (or a combination of loss offset election and subvention payment). A subvention payment is a deductible payment from the profit company to the loss company in return for the use of the loss. The subvention payment is assessable income to the loss company (thus it extinguishes the loss company’s tax losses).

2.11 There are several conditions that must be met in order for companies to undertake a loss offset. In particular, the two companies must have at least 66 percent common shareholding interests from the start of the income year in which the tax loss arose to the end of the income year in which the tax loss is grouped.

2.12 The policy underlying loss grouping is essentially a consolidation or “single economic entity” policy. If two companies have 100 percent common ownership, it is economically equivalent to conducting the same two activities through a single company. If the ultimate shareholders have a choice between operating an identical enterprise through a single company, or through two companies, tax consequences should not distort the decision – the choice should be made for commercial reasons. For historic reasons,[1] this consolidation policy was extended to 66 percent commonly owned companies for the loss grouping regime only. In contrast, the inter-corporate dividend exemption applies only to a true “single economic enterprise” scenario – that is, within a wholly owned corporate group (100 percent common ownership).

Interaction of the two regimes

2.13 Issues arise, however, when the two regimes interact and the ownership is greater than 66 percent but less than 100 percent. Losses can be grouped but tax is also reduced with consequently fewer imputation credits generated. If the profit company subsequently wishes to pay an imputed dividend to one of its corporate group shareholders the profit company may have insufficient imputation credits to be able to fully impute the dividend.[2]

2.14 This is only problematic when there is a minority shareholder in the profit company, that is, common shareholding between the loss company and profit company is 66 percent or higher, but less than 100 percent and the profit company does not have additional imputation credits from past tax payments. If the loss company and profit company are within a wholly owned group of companies (100 percent commonly owned), the inter-corporate dividend exemption means that lack of imputation credits to fully impute dividends is not an issue.

2.15 For shareholders in a non-wholly owned profit company, the receipt of an unimputed or partially imputed dividend is an issue for them as they will be required to pay extra tax. This is particularly the case when there is an unrelated minority shareholder who may not have benefitted from the loss grouping, but still suffers as a result of the reduced imputation credits.[3]

2.16 As discussed above, this issue arises because the underlying policy approach to groups of companies for the dividend regime and the loss grouping regime differs.

Example

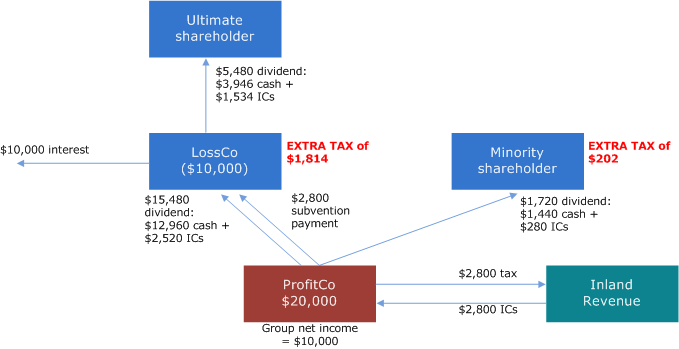

2.17 Diagram 1 sets out an example of how this issue arises in practice. It shows a loss company which has a 90 percent shareholding in a profit company (which makes those companies eligible to group losses). It shows the profit company making a subvention payment for the use of the loss company’s losses,[4] and the subsequent dividends paid out by the profit company being only partially imputed. This results in the shareholders of the profit company having to pay extra tax on the dividends they receive, which they would not have had to pay if the loss grouping had not occurred and tax had been paid at the company level. The minority shareholder has not benefited from the loss offset, and, in fact, has been disadvantaged relative to the situation where no loss offset had occurred.

Diagram 1: A loss offset by a 90 percent shareholding company[5]

2.18 The following tables set out the relevant entries in the imputation credit accounts of the loss company and the profit company.

| Debit | Credit | |

|---|---|---|

| Dividend received | $2,520 | |

| Tax paid | $1,814 | |

| Dividend paid | ($1,534) | |

| Balance | $2,800 | |

| Debit | Credit | |

|---|---|---|

| Tax paid | $2,800 | |

| Dividends paid | ($2,520) ($280) |

|

| Balance | $0 | |

2.19 This example highlights the outcome when the loss grouping rules interact with the imputation regime. Namely, the overlay of the imputation regime effectively claws back some of the benefit afforded by the loss grouping rules. The shareholders pay extra tax of $2,016 ($1,814 by the majority shareholder and $202 by the minority shareholder). The minority shareholder is worse off than if the loss grouping had not occurred and the profit company had paid the full amount of tax. The majority shareholder is also worse off than if the loss grouping had not occurred, provided they could have eventually used the loss against other income.

2.20 Another way of looking at this, is that if the activities of ProfitCo and LossCo were carried on directly by the corporate shareholders, the total tax payable on the $10,000 net income would be $2,800 (an effective tax rate of 28 percent). However, because ProfitCo and LossCo are not part of a wholly owned group, the interaction of the loss grouping and imputation rules means that the total tax payable on the $10,000 of group net income is $4,816 (although additional imputation credits are generated).

Why is there a need to address this issue?

2.21 Officials have been advised that the interaction of the regimes described above may be causing problems in practice and distorting economic decisions. For example, a company considering acquiring 66 percent or more of the shares in another company is currently incentivised to acquire 100 percent of the target company in order to access the inter-corporate dividend exemption to avoid the issue identified above which ultimately results in an additional tax cost to shareholders. This suggests that interaction of these two regimes could be distorting potential business combinations. This could provide an incentive to shut out minority investors, and could prevent an owner/operator or key employees retaining a stake in the company when they sell more than 66 percent of that company to an investor.

2.22 Shareholder companies may be more likely to be in tax loss when they have recently undertaken a debt-financed acquisition of another company because the acquisition vehicle normally bears the interest costs on the debt funding. This suggests that this issue may be more prevalent in the context of mergers and acquisitions.

2.23 Officials have also been advised that this is one factor that could act as a barrier to partial corporate listings on the New Zealand stock exchange (NZX) – because losing 100 percent common ownership via listing means the inter-corporate dividend exemption is no longer available.

2.24 Thus removing this issue for commercially desirable transactions could have flow-on benefits for the New Zealand economy – both in terms of facilitating New Zealanders retaining a minority stake in a successful New Zealand company and increasing the attractiveness of listing on the NZX resulting in a deeper capital market.

1 The grouping of profits and losses of companies with “substantially the same” shareholders or under common control was originally an anti-avoidance provision that was introduced when New Zealand had a progressive company tax rate; see section 141 of the Land and Income Tax Act 1954. This was designed to prevent a business being broken into a number of separate companies to avoid the higher marginal tax rates. Following amendments in 1968, the Commissioner no longer had to invoke avoidance to assess group companies (now defined to be companies with two-thirds common ownership) at the tax rate that would apply to the aggregate taxable income of the group. The corollary of this automatic aggregation of group income was the ability of group companies to use subvention payments to group tax losses. It was originally proposed that grouping of income would occur at 50 percent commonality and subvention payments could be made at 75 percent commonality. Ultimately, the two-thirds threshold was adopted for both income and losses. New Zealand’s 66 percent commonality threshold for loss grouping is substantially lower than other OECD countries – notably Australia which only allows grouping within a consolidated group (which requires 100 percent common ownership).

2 This will ultimately depend on whether the profit company has additional imputation credits from tax paid on other profit streams.

3 We note however that minority oppression rules in company law would generally require that the loss offset was done in a manner that does not disadvantage the minority shareholders.

4 In the example, the full $10,000 tax loss is transferred from LossCo to ProfitCo via a combination of a 28 percent subvention payment and a loss offset election for the remaining $7,200 tax loss.

5 All shareholders are assumed to be on a 28% tax rate to keep the diagrams and examples as simple as possible.