The taxation of land-related lease payments

Overview

Currently, the Income Tax Act 2007 provides for the tax treatment of certain land-related lease payments. For example, lease premiums, lease inducement and lease surrender payments are generally taxable and tax deductible under the Act. In absence of specific provisions, the tax treatment of other land-related lease payments is determined under general provisions and principles.[7]

Since the Act does not provide comprehensive coverage of all land-related lease payments, similar lease payments can be treated differently for income tax purposes, which can have the effect of distorting business decisions.

An officials’ issues paper, The taxation of land-related lease payments, released in April 2013, sought feedback on proposals to introduce a broad reform to achieve a coherent and consistent tax treatment of all land-related lease payments. In particular, the issues paper suggested making commercial land-related lease payments taxable and deductible by introducing a bright-line rule of 50 years for leases and licences of land. Commercial leases or licences of land lasting less than 50 years would therefore have been put on revenue account. Leases and licences of land lasting 50 years or more would have been put on capital account, which would provide a similar tax treatment to most freehold land.

Following public consultation, the Government decided to introduce a targeted reform to address specific revenue risks with lease transfer payments (that is, received by an exiting tenant for transferring a lease to an incoming tenant).

The bill proposes to tax, from 1 April 2015, certain lease transfer payments, which are substitutable for taxable lease surrender and lease premiums payments. This bill also proposes a number of technical amendments to tax law relating to leases and licences of land to provide consistency and certainty.

LEASE TRANSFER PAYMENTS

(Clauses 9 and 123(23))

Summary of proposed amendment

The proposed amendment taxes certain lease transfer payments that are substitutable for taxable lease surrender payments and lease premiums.

Application date

The amendment will apply from 1 April 2015.

Key features

New section CC 1B extends section CC 1B to include certain lease transfer payments that are substitutable for taxable lease surrender payments in section CC 1C and taxable lease premiums in section CC 1.

A lease transfer payment will be taxable in following situations:

- The lease transfer payment is sourced directly or indirectly from funds provided by the owner of the estate in land from which the land right is granted; such a payment is substitutable for a lease surrender payment.

- The person purchasing the lease is associated with the owner of the estate in land from which the land right is granted; the lease transfer payment is substitutable for a lease surrender payment.

- The vendor of the lease is associated with the owner of the estate in land from which the land right is granted; the lease transfer payment is substitutable for a lease premium.

Background

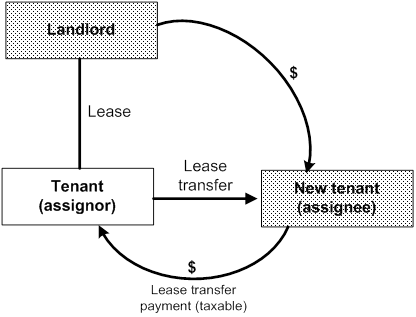

Lease transfer payments are generally received by an exiting tenant (assignor) from a new incoming tenant (assignee), for the transfer or assignment of a lease. For income tax purposes, the payment is generally non-taxable to the exiting tenant.

The current non-taxable status of lease transfer payments, in tandem with taxable lease surrender payments,[8] can distort commercial decisions when tenants exit a lease. As lease transfer payments are generally not taxable, it would be tax advantageous for a tenant to exit a lease by transferring the lease to a third party for a tax-free lease transfer payment, rather than surrendering it to a landlord for a taxable lease surrender payment.

From the exiting tenant’s perspective, there is no economic difference between surrendering the lease to the landlord and transferring it to a third party. The effect is the same – the tenant exits the lease and receives consideration for it. Treating similar payments differently for income tax purposes distorts business decisions and results in economic inefficiency and unfairness.

Example

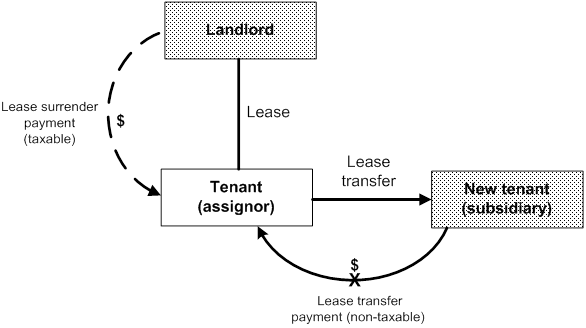

On 1 April 2015, a landlord and a tenant enter into a 10-year lease. After three years, the landlord expands its business to retail, by setting up a subsidiary company. The landlord wishes the tenant to exit the lease so that the subsidiary company can use the premises to carry on its retail business.

If the landlord pays a lease surrender payment to the tenant, the payment is taxable to the tenant and deductible to the landlord.

A subsidiary company of the landlord and the tenant enter into an agreement to transfer the lease. The subsidiary company pays the tenant $100,000 for the transfer.

Under the current rules, the lease transfer payment of $100,000 is deductible to the subsidiary company over the remaining seven years under the depreciation rules. The lease transfer payment is non-taxable to the exiting tenant. The exiting tenant is $28,000 ($100,000 x 28%) better off than receiving a lease surrender payment from the landlord.

The revenue risk increases when the commercial property market tightens – that is, when there is a shortage of business premises in economic upturns. This is because lease transfer payments from new tenants or lease surrender payments from landlords tend to occur more often when leases become valuable in a tight commercial property market. For example, prospective tenants or landlords would be more prepared to pay existing tenants for the transfer or surrender of a lease.

Following public consultation, the Government decided to tax certain lease transfer payments as a base-protection measure – that is, to prevent non-taxable lease transfer payments being substitutable for taxable lease surrender payments or lease premiums.

Detailed analysis

The tax treatment of lease transfer payments

The new rules extend section CC 1B to include certain lease transfer payments. This extension is intended to be a targeted base-maintenance measure.

If a person (the payee) derives an amount, in relation to a land right, as consideration for the transfer of the land right from the holder of the land right to another person, the amount will be taxable to the payee (new sections CC 1B(1)(b) and (2)). The land right must be a right that is a leasehold estate or a licence to use land.

The term “leasehold estate” is defined broadly in section YA 1 to include any estate, however created, other than a freehold estate.[9] The charging provision, therefore, does not apply to payments for a freehold estate in land, such as the proceeds from the sale of land.

Despite this broad charging provision for lease transfer payments, most lease transfer payments will not be taxable by satisfying the following conditions listed in new section CC 1B(3):

- the payee is the holder of the land right (for example, the exiting tenant);

- the amount is consideration for the transfer of the land right to the person paying the amount (for example, the new tenant);

- the amount is not sourced directly or indirectly from funds provided by the owner of the estate in land from which the land right is granted; and

- each of the payee and the person paying the amount is not associated with the owner of the estate in land from which the land right is granted.

Payments derived in situations when these conditions are not satisfied will be taxable to the payee. If a lease is transferred as part of a business transfer, consideration for goodwill attaching to the land will be taxable to the payee; however, consideration for business or personal goodwill will not be subject to the charging provision.

Situations involving lease transfer payments that are covered by the proposed section CC 1B are payments that are substitutable for taxable lease surrender payments in section CC 1C and taxable lease premiums in section CC 1.

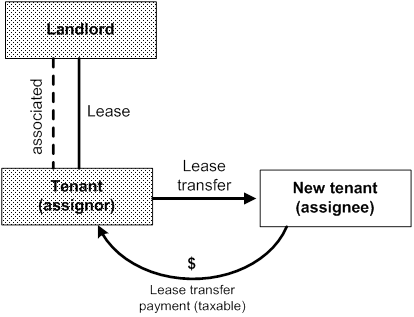

There are two situations when lease transfer payments that are substitutable for lease surrender payments will be taxable to the payee. They are:

- if the amount is sourced directly or indirectly from funds provided by the owner of the estate in land from which the land right is granted.[10]

- if the person paying the amount is associated with the owner of the estate in land from which the land right is granted.

An exception for a tenant or a licensee of residential premises will apply to the two situations described above. The amount is not income if the payee is a natural person (individual) and derives the amount as a tenant or licensee of residential premises whose expenditure on the residential premises does not meet the requirements of the general permission (proposed section CC 1B(4)(a)). This exclusion is intended to provide a consistent tax treatment with that for lease surrender payments in section CC 1C.

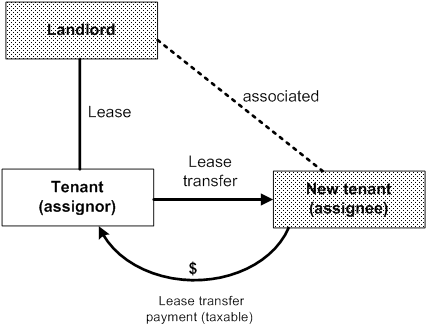

Another situation when lease transfer payments will be made taxable is payments that are substitutable for lease premium payments. In particular, if the payee is associated with the owner of the estate in land from which the land right is granted, lease transfer payments will be taxable.

This would prevent a landlord setting up a lease with a low rent with their associate and, as part of this arrangement, the associated tenant transfers the lease to a non-associated tenant and receives a non-taxable lease transfer payment.

Taxing a lease transfer payment in such situation will supplement the existing anti-avoidance provision in section GC 5, which allows the Commissioner to set an adequate level of rent for leases between associates.

Lease transfer payments received for residential premises will also be taxable if the payee (the tenant) is associated with the owner of the estate in land from which the land right is granted (proposed section CC 1B(4)).

The definition of “land provisions” in section YA 1 will be amended so that the definition of “associated person” applying in new section CC 1B is the one applicable to land provisions.

If a person receives a lease transfer payment on behalf of another person, the current nominee rules in section YB 21 apply to treat the amount as derived by that other person.

An amount that is subject to the existing capital contribution rules will not be subject to the charging provision (proposed section CC 1B(5)). A capital contribution will continue to be income under section CG 8 and spread evenly over 10 years unless the payee chooses to reduce the cost base of the depreciable property under section DB 64.

Timing of income

The timing provision in section EI 4B applies to the amount of income under section CC 1B. Under that provision, the allocation of income is affected by when the income is derived in relation to the spreading period.

The exiting tenant (assignor) who receives a lease transfer payment has no remaining period over which to spread the amount of income under section CC 1B. Therefore, the amount of income will be allocated to the income year in which the amount is derived.

PERMANENT EASEMENTS

(Clause 8)

Summary of proposed amendment

The proposed amendment excludes a payment for a permanent easement from being taxable to a landowner under existing section CC 1.

Application date

The amendment will apply from 1 April 2015.

Key features

Proposed section CC 1(2C) provides that if an owner of a fee simple estate in land derives an amount as consideration for the grant, for the duration of the estate, of an easement over the land, the amount will not be income of the owner. The purpose of this specific exclusion is to align the tax treatment of a permanent easement (or a perpetual right of way) with that for freehold land under the existing section CC 1.

Accordingly, a payment for a permanent easement will not be taxable to the owner of land (the grantor) under section CC 1,[11] and a payment for a permanent easement will not be deductible to the payer (the grantee) under the depreciation rules.

Background

Section CC 1 applies broadly to tax income from land by providing that amounts derived from land by a landowner are taxable even if the amounts are traditionally categorised as capital in nature – for example, a lease premium. A payment for a permanent easement is currently taxable to a landowner under section CC 1.

On the other hand, a payment for a permanent easement is generally non-deductible to the payer (the grantee) under the depreciation rules. Generally, a permanent easement does not meet the definition of depreciable property under section EE 6; in particular, in normal circumstances, a permanent easement is not reasonably expected to decline in value.

PERPETUALLY RENEWABLE LEASES (“GLASGOW” LEASES)

(Clause 53)

Summary of proposed amendment

The proposed amendment excludes a perpetually renewable lease from being depreciable property.

Application date

The amendment will apply from 1 April 2015.

Key features

Section EE 7 will be amended to exclude a lease of land with a perpetual right of renewal from being depreciable property. The purpose is to treat a perpetually renewable lease similarly to freehold land under the depreciation rules. Accordingly, depreciation deductions will not be available for a perpetually renewable lease.

Background

Perpetually renewable leases last for a certain duration (for example, 7, 10 or 21 years), but are renewable in perpetuity at the option of tenants. They are commonly known as “Glasgow” leases. They are typically for the bare land only and tenants generally own the improvements on the land. Rents on these leases are reviewed periodically (usually to a market rate).

Under the current rules, “the right to use land” is contained in the list of depreciable intangible property in schedule 14 of the Income Tax Act 2007. Usually, a commercial tenant of a lease can claim depreciation deductions for their cost to acquire the lease (that is, a lease premium or lease transfer payment) over the term of the lease.

However, a tenant under a perpetually renewable lease may not claim depreciation deductions during the term of the lease because these leases have a perpetually renewable lease period. The tenant, however, may be able to claim a depreciation loss when the perpetually renewable lease is sold for less than its adjusted tax value if the lease meets the definition of “depreciable property” in section EE 6 – that is, in normal circumstances, the lease might reasonably be expected to decline in value.

Note that a payment for a perpetually renewable lease continues to be taxable to a landowner under section CC 1. This payment (for example, a lease premium) is easily substitutable for taxable rent payments on a perpetually renewable lease that are periodically reset to market levels.

CONSECUTIVE LEASES

(Clauses 56, 123(23) and 123(24))

Summary of proposed amendment

The proposed amendment treats consecutive leases of land as a single lease for depreciation purposes.

Application date

The amendment will apply from 1 April 2015.

Key features

Section EE 67 will be amended to include consecutive leases in the existing definition of “legal life” for a lease and licence to use land. The definition of “legal life” is used to determine the annual depreciation rate for an item of fixed-life intangible property, such as a lease of land, in section EE 33.

If consecutive leases over the same parcel of land are granted to a person or an associated person at the same time, the term of a lease owned by the person will also include the terms of consecutive leases owned by that person or an associate. This will have an effect of treating consecutive leases as a single lease.

Any genuinely subsequently negotiated leases or licences of land will not be counted towards the legal life of a lease. Consecutive leases would need to be acquired by the person or associated person at the same time to be counted towards the legal life of a lease.

This is intended as an anti-avoidance measure to prevent the timing of depreciation deductions for the cost of acquiring a lease (a lease premium or lease transfer payment), being accelerated by entering into consecutive leases. If consecutive leases are entered into around the same time (such as one day apart), the general anti-avoidance provision in section BG 1 may apply to counter any transactions that attempt to circumvent this measure contrary to the policy intent.

Example

On 1 April 2015, A Ltd and its associates, B Ltd and C Ltd, enter into three separate leases for the same parcel of land to take effect immediately after one terminates. The first lease commences on 1 April 2015. Each lease lasts for 10 years.

| Lease | Commencement date | Lease ownership | Term of the lease |

| 1 | 1 April 2015 | A Ltd | 10 years |

| 2 | 1 April 2025 | B Ltd | 10 years |

| 3 | 1 April 2035 | C Ltd | 10 years |

- A Ltd’s interest (owner’s interest) in the lease will be treated as lasting for 30 years, which includes both B Ltd and C Ltd’s interests in the lease.

- B Ltd’s interest (owner’s interest) in the lease will be treated as lasting for 20 years, which includes C Ltd’s interest in the lease.

- C Ltd’s interest (owner’s interest) in the lease lasts for 10 years as there is no consecutive lease.

The definition of “land provisions” in section YA 1 will be amended so that the definition of “associated person” applying in section EE 67 is the one applicable to land provisions.

Also, paragraph (d)(v) of the definition of “lease” in section YA 1 will be amended to remove the Commissioner’s discretion to determine consecutive leases for the purposes of personal property lease payments. A similar definition to the one that is proposed for depreciation purposes in section EE 67 will be adopted to provide certainty and consistency.

Background

Consecutive leases are multiple leases for the same parcel of land that are granted to a person or an associated person at the same time, and are linked to take effect immediately after one terminates. Under the current rules, depreciation deductions on a lease could be accelerated by entering into consecutive leases, including involving associated persons, rather than a single lease.

RETIREMENT VILLAGE OCCUPATION RIGHTS

(Clause 123(25))

Summary of proposed amendment

The proposed amendment excludes an occupation right agreement as defined in the Retirement Villages Act 2003 from the financial arrangement rules.

Application date

The amendment will apply from 1 April 2015.

Key features

Paragraph (f) of the “lease” definition in section YA 1 will be amended to include an occupation right agreement as defined in the Retirement Villages Act 2003. This way, retirement village occupation rights will be treated as an excepted financial arrangement in section EW 5(9), and accordingly excluded from the financial arrangement rules.

This amendment is intended to align the treatment of retirement village occupation rights with leases of land under the financial arrangement rules, and to provide certainty that retirement village residents are not subject to these rules.

Background

Leases are currently excluded from the financial arrangement rules because they are excepted financial arrangements under section EW 5(9). However, retirement village occupation rights that are licences to occupy are currently regarded as financial arrangements because they are not a lease for the purposes of financial arrangement rules as defined in section YA 1.[12]

Treating certain retirement village occupation rights as financial arrangements is undesirable from a policy perspective. In particular, if certain retirement village occupation rights are subject to the financial arrangement rules, there may be tax consequences for a retirement village resident.[13]

Note that Determination S16, which was issued by the Commissioner of Inland Revenue in 2010, applies to certain retirement village occupation rights that are leases resulting in the financial arrangement rules not applying to such arrangements. However, a legislative amendment in this area would provide greater certainty and ensure that all occupation right agreements under the Retirement Villages Act 2003 are excluded from the financial arrangement rules.

7 Generally, payments that are revenue in nature, such as receipts or expenditure derived or incurred in the ordinary course of business, are treated as taxable income and tax deductible expenditure. Generally, payments that are capital in nature are treated as non-taxable income and non-deductible expenditure.

8 Lease surrender payments are taxable under section CC 1C of the Income Tax Act 2007.

9 For income tax purposes, an interest in land has the same meaning as an estate in land.

10 Note that the payment from the landlord to the new tenant for the lease transfer is deductible to the landlord under section DB 20B and taxable to the new tenant under existing section CC 1B.

11 Note that the land provisions in sections CB 6 – CB 23B continue to apply to permanent easements.

12 See paragraphs (d) and (f) of the definition of “lease” in section YA 1.

13 The existing financial arrangement rules shift financial benefits from the transaction from one party to another. Consequently, under certain retirement village occupation rights arrangements, deductions may be allowed to a retirement village operator and assessable income may arise to the resident. This tax outcome would not generally have been contemplated by the contracting parties at the time of the transaction.